Last Updated on March 12, 2024 by Lukas Rieder

Integrated planning and control includes coordinating plans because holistic coordination creates a central basis for achieving desired results. For this reason, and in order to derive the detailed requirements for the integrated overall system, the mutual dependencies between the various subsystems of planning are dealt with below.

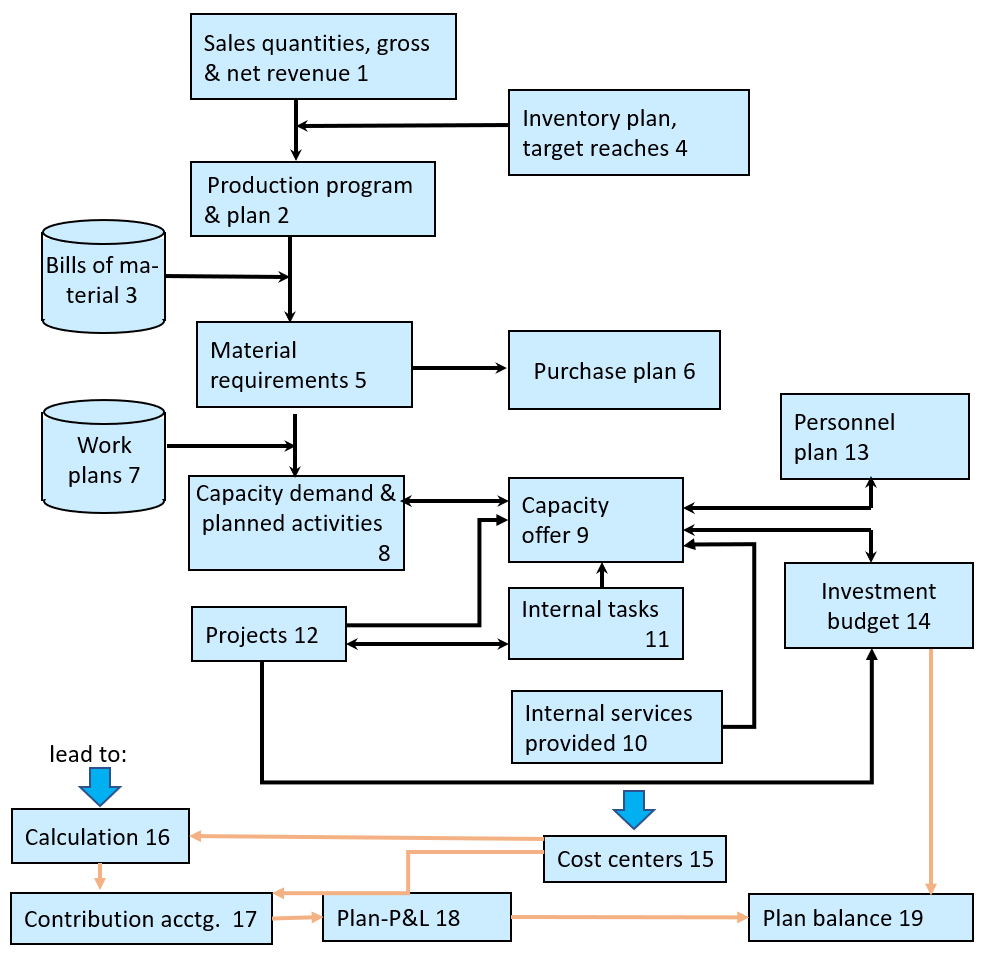

Starting point are the results from the planned sales volumes and net sales/net revenue (1 in the following exhibit). Using this information, the person responsible for annual production planning derives the production program, also called the rough plan (2). Taking the planned sales quantities per item into account, the task is to determine how many units of which finished product are to be produced.

The following factors play a role in determining this:

- Bills of material (3): An example of a bill of material can already be found in the post “Pizza Dough and Management Accounting“. It shows which raw materials have to be provided in what quantities for the pizza dough.

- Batch sizes, setup material and scrap (3). These details are also included in the pizza dough example (see respective post). The dough should be enough for four pizzas of 20cm diameter, some flour is needed to roll out the dough and the cuttings that result from cutting into the round shape are actually scrap, which could be used for a small decorative dough figure, but otherwise ends up in the waste.

- Inventory targets in terms of quantity, value, and readiness for delivery at any time (4). This is where different interests collide: The production manager wants to be able to produce as large batches as possible so that the consumption for setup and scrap is distributed over as many finished units as possible. The purchasing officer also has an interest in large batches because this enables him to order larger quantities and thus negotiate more favorable purchase prices. The salespersons always want to have enough finished products in stock to satisfy every customer need immediately and thus generate sales. The CFO, however, does not like large lots because he fears that on average there are more units in inventory and therefore more value. The CFO has to finance these stocks with bank loans or capital injected by the owners. In addition, the return on investment (profit before deduction of interest and taxes in relation to the invested assets) looks worse if the profit remains the same but the inventory values increase. The latter makes the company appear less profitable to external observers (bankers and potential investors). The CFO will therefore want lower inventory values.

Based on this discussion, the production planner determines the planned quantity for each item to be produced. This results in the production plan of the year. By multiplying the planned quantity per item with the standard quantities in the bills of material, the material requirements for raw materials and semi-finished products are calculated. Summarized for each raw material, this results in material requirements planning (5). This enables the person responsible for purchasing to negotiate prices and conditions with potential vendors (6). The latter are very interested in concluding annual allotments, because it enables the suppliers to better align their own capacities with the anticipated demand and thus also to produce less costly.

If the quantities to be produced per item are known from the production program, the time requirements can be planned. The prerequisite for this are the work plans (7). In the post Pizza Dough and Management Accounting the individual processes for the production of the pizza dough were also described. The work plan also specifies the working times per process step, which must be observed if skilled workers carry out these operations. In this example, setup and cleanup times are also to be expected, which can be clearly assigned to the product “pizza dough”. The planned production quantities are multiplied by these standard times item by item. The setup times and the allowed processing times for scrap are multiplied by the planned number of lots per item.

By adding up all processing, setup and scrap times, the planned employment of the cost centers directly involved in the production process is calculated. The planned operating capacity is required for cost center planning on the one hand and for determining the personnel plan (13) and machine capacities (9) on the other.

Several service centers usually enable all other cost centers to work at all. Examples are: Workshops, internal transports, energy supply (electricity, steam, compressed air). Their work and costs must also be planned, since they depend on the requirements of the cost centers receiving them (internal services provided (10)).

The necessary working hours and machine capacities for the planned projects (12) are planned accordingly.

Internal tasks (12) include all activities necessary for the upkeep of an organization but their consumption is only indirectly caused by the planned production. This includes all management, planning and administrative work including sales, information technology, building and maintenance, personnel administration, and accounting.

The personnel requirements plan (13) and the investments (14) required to implement the overall plan can only be completed at the end of the overall planning process, since the upstream areas determine the requirements.

For the design of the management control system, it should be noted that up to now, without exception, quantities, activities, times, and capacities have been mentioned. Only in management accounting are these units combined with money and value to provide the overall view.