Last Updated on March 12, 2024 by Lukas Rieder

Plan Internal Services to be provided

Internal services are provided when a receiving cost center directly orders services (activities) from another cost center. Such an order can be placed explicitly or be the direct consequence of the activity level of the ordering cost center. The supplying area is therefore responsible for providing the service.

Examples:

-

- A car of the sales department is damaged and repaired in the company’s own garage (the order could also have been placed externally).

- Every 100 operating hours the repair department has to check the dimensional accuracy of the rolls in the Rolling and Punching cost center for four hours and replace the rolls if necessary.

- The maintenance group receives an order to rebuild the entrance of the reception building according to the latest safety standards.

- The energy supply division supplies all other divisions of the company with electricity, water, and compressed air. Consumption is directly dependent on the equipment installations and on the performance of the receiving cost centers. It can be measured using meters or calculated using consumption tables.

- Every tenth production order must be checked in the internal laboratory for compliance with all quality regulations.

In these cases, the ordering cost center is the trigger for the production of the service, either through an explicit order or through an automatic relationship between the service provided in the ordering area and the service delivered by the service area (2,4,5 above). The originator of the service procurement is always the delivering party. The ordering party should plan (in cooperation with the internal supplier) the services for a year, so that the personnel and machine capacities required by the internal supplier can be determined from this information.

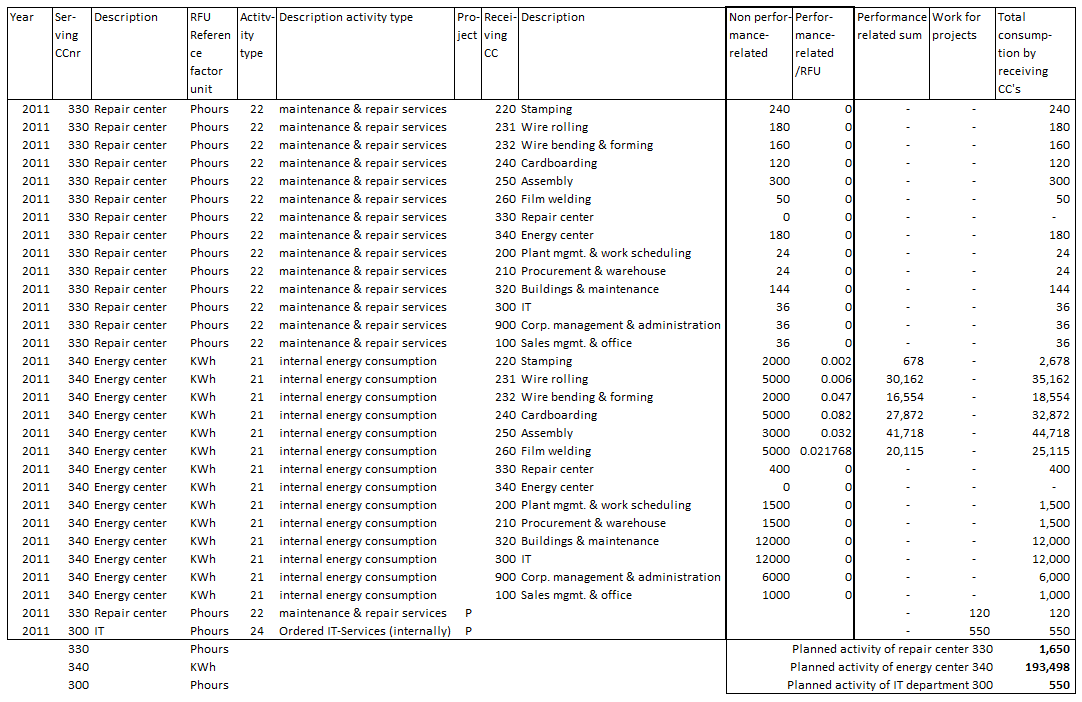

In the example company Ringbook Ltd., the genuine internal exchange of services is planned in the following table:

The consumption estimates of the receiving cost centers are collected and converted to the personnel hours or kWh required. A distinction must be made between which consumption is dependent of the activities of the receiving cost centers and which is independent (mainly calendar-driven). Totaling the values in the last column gives the planned activity levels of the internal service providers.