Last Updated on March 12, 2024 by Lukas Rieder and David Moser PhD

The example company manufactures brake valves for precise moving and holding of heavy loads. These valves, of which there are approximately 3,000 types, are integrated into the example company’s own products as well as into those of other manufacturers.

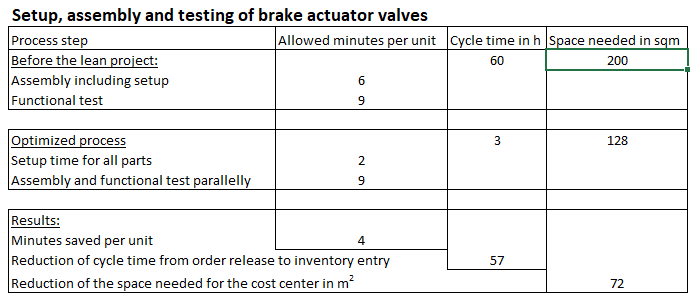

Lower Proportional Costs with Lean Production

The mission was to reduce proportional costs with Lean Production, while also realizing shorter lead times and lower average inventories in the work in process and finished goods inventory accounts.

This goal was mainly achieved by redesigning the production flow. All individual parts to be assembled into a specific brake valve are now prepared on a slide in a setup line and delivered via conveyor to the final assembly station. The manual final assembly and the computer-aided test process were merged into one overall process (during the test process, the specialist assembles the next valve and determines the test result).

Increase flow and reduce processing time

At the end of the test phase, the following results were measured:

Result: Lower product costs, shorter lead time, less space required, higher production capacity.

Since the material input (semi-finished and purchased parts) has not changed, only the standard times in the work plans have to be adapted for the standard cost estimate of the products. The project implementation leads to the reduction of the standard time per piece of 4 minutes. Assuming that an employee in this cost center, including social benefits, costs 85,000 per year and works a net 1,700 hours per year, this results in an hourly rate of 50.- and a minute rate of EUR 0.833. The proportional manufacturing costs per brake valve are therefore reduced by EUR 3.333, since 4 minutes are saved. The standard proportional manufacturing cost also decreases by EUR 3.333 in the next plan year. This development increases competitiveness and decreases the value of work in process and inventory. As a result, total assets are smaller and there are reduced interest costs.

If the management accounting system is set up in the form of proportional standard cost accounting, the implementation success of the lean project can be read directly from the target to actual variances on a monthly basis. If the target times from the lean project are not adhered to, working time variances occur. If the actual order-related material consumption does not correspond to the planned consumption according to the bill of materials, material consumption variances occur. Similarly, variances in setup times and quantities or yield rates can also be measured.

Improved throughput and less space needed

The effect of the reduction in throughput times in terms of value cannot be answered unambiguously, as it depends above all on customer behavior. If customers can be supplied more quickly as a result of this time gain, this can lead to additional sales and possibly also to new customers. Whether these additional sales will be made is usually difficult to assess and should therefore not be included in sales planning. In any case, the customer benefit increases due to faster delivery.

The reduced space requirement only has a financial consequence if suitable space becomes a bottleneck in the case of extensions or conversions and, as a result, new rooms have to be built or rented. Any resulting cost increase would have to be planned in the enlarged cost center. (Note: In decision-relevant management accounting, the space costs are not allocated to the products, since they are fixed costs that continue to be incurred even if no more production takes place).

David Moser PhD

Dr. David Moser is co-founder and managing partner of Wertfabrik AG. With a doctorate in physics, he has many years of experience, including in the areas of Lean Enterprise, Lean Administration, Shopfloor Management and coaching of executives. Before founding Wertfabrik, he was Managing Director at HARTING AG in Biel/Switzerland and most recently Managing Director and Senior Partner at STAUFEN AG also in Switzerland. Today, the specialist for process optimization is active as a consultant and speaker for numerous industries.