Last Updated on March 12, 2024 by Lukas Rieder

Many executives complain that planning takes too long. This is normal. After all, planning work takes time,

-

- which is lacking in selling, producing, administering,

- is needed for dealing with the uncertain future and making assumptions,

- is needed for mutual coordination and scheduling, as well as

- is needed to determine what results are to be reached, when they are to be achieved, and what must be ready for that to happen.

Just working ahead is less challenging than agreeing on objectives and planning to achieve them. But without planning, overarching coordination is lacking and results, up to and including the payment of salary, become haphazard.

Integrated and comprehensive planning is a prerequisite for the survivability of any organization (including a family). The question is which planning content is relevant and when, and how to schedule the planning process in the annual calendar so that the desired results can really be achieved.

Planning takes too long

Those who are to determine objectives or plan values want to know the actual state, i.e. the starting point, and the near future to be expected as precisely as possible. This leads to delaying the definitive determination of objectives as long as possible. It is therefore advisable to record the various sub-plans with their required completion dates in a planning calendar.

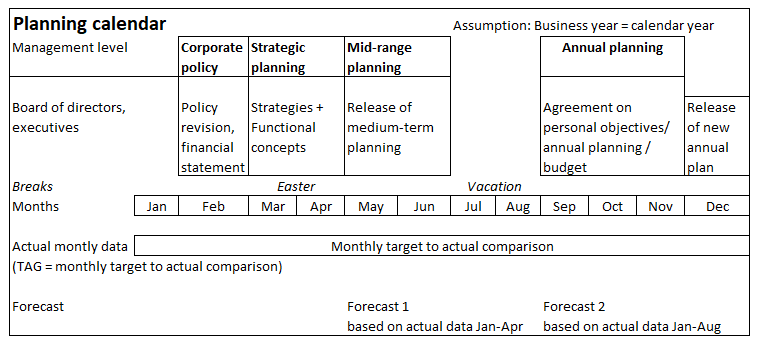

If the complete development of the plans is calculated back to annual targets and plans starting from the release decision, the following ideal-typical planning calendar results (assumption: fiscal year = calendar year):

-

- In order to be able to start tracking the new targets right at the beginning of the year, the annual objectives for each person should have been agreed and released at the end of the previous year. In order for the Executive Board or the Board of Directors to be able to give this release, the mutually agreed objectives and budgets of all levels and areas for the next year must be known in good time. This release usually takes place shortly before Christmas. If the top management bodies approve the submissions, this means the release of the following year’s targets and plans at all levels.

- The actual annual planning should therefore begin in September, as it requires the most coordination and therefore also the most time. Because it is necessary to plan from the sales markets into the company, it follows that sales/revenue planning is at the beginning. By the end of October at the latest, the planned net revenues, the capacities required (personnel and equipment) and the main projects for the following year should be determined so that cost center planning and the consolidation of the plans can take place in November. For this purpose, the planned prices for goods and services to be procured must also be determined by the end of October so that standard cost calculations are possible. The transmission of the entire planning to the top management or to the administrative and supervisory boards must take place in the first days of December so that the latter can prepare their meeting.

- The updated medium-term planning must be ready before the summer break (around the end of June) so that the management can decide on it and so that the controller can publish the planning letter with the basic principles and key figures for the next annual planning by the end of August. Consequently, the medium-term planning should be updated in May/June (especially multi-year projects, R+D orders, capacities, training and further education, investments), as it contains essential benchmarks for the next annual planning.

- This requires that strategy revision has to take place in March and April. Top management and the Administrative/Supervisory board must approve the updated strategies, because they in turn provide inputs for medium-term planning.

- In February/March, the final financial statements for the previous year are usually ready for approval by top management. At this meeting, it is also important to update the corporate policy (management concepts, vision and mission statement), as any changes have an impact on strategic planning.

- The forecasts provide an essential input for the preparation of the budgeted accounts, especially with regard to expected sales and purchase prices. Preparing forecasts means drawing up estimates of price and volume changes in the sales and procurement markets, which is also time-consuming. Consequently, managers must be burdened as little as possible with forecast preparation. Contrary to the accounting standards for listed companies (IFRS and US GAAP), which require a forecast every quarter, we recommend that only two forecasts be commissioned annually:

-

-

- The first should be prepared on the basis of actual data from January to April, because Easter is celebrated once in March and the other time in April.

- The second forecast is to be prepared on the basis of actual data from January to August, because this is when most of the vacations are taken. This second forecast thus also forms an important input for the planning of the next year, which should begin in September as described.

- There is no need for a further forecast, as this would refer to the first four months of the planned year. However, the corresponding data are already included in the annual planning.

-

The need for forward thinking means that managers at all levels are involved in planning for most of the year. This is because ensuring that the skills, capabilities and resources are available on time requires different lengths of time as well as answering different questions in the planning stages to process the determinations in the planning stages.