Last Updated on March 12, 2024 by Lukas Rieder

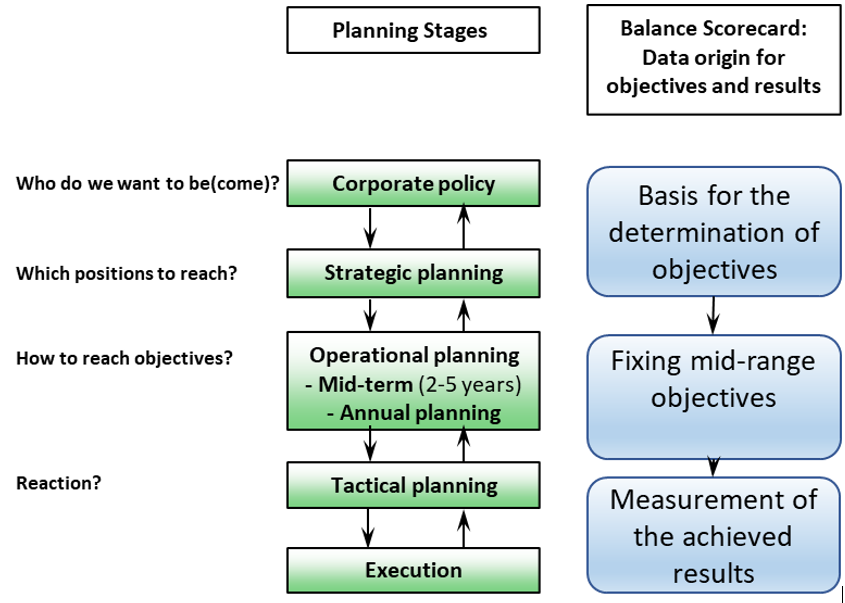

The Balanced Scorecard is intended to measure and assess how well the strategy has been implemented during the reported period. In the Management Control System, different planning levels are distinguished (see the post “The Main Questions of each Planning Stage”). Corporate policy expresses what purpose the company should fulfill from the point of view of the owners and what guidelines for development they envisage. The strategies are developed from this. Formulated corporate policy and strategies are prerequisites for the introduction of the BSC.

In the post “Strategy and Functional Concepts”, it was explained that there is hardly one common strategy for the entire company because each independent product/market combination can appear differently in its respective market. The strategic plans and goals are thus to be formulated by strategic business unit, SBU. This also corresponds to the recommendation of Kaplan and Norton in The Strategy Focused Organization, p. 45f.”.

An SBU is to be formed if different product/market combinations occur with their own corresponding pricing and offering and possibly even the unique selling proposition is different. This leads to a strategy per SBU and consequently to a specific BSC for this business unit.

In the post “Strategy and Functional Concepts”, we recommend answering six question groups when creating and documenting an SBU strategy:

Basic Idea, Framework, Assessment, Objectives, Plan of Measures, Critical Assumptions.

The objectives are the starting point for the creation of the BSC, the plan of measures is the input for operational planning. The critical assumptions are to be scrutinized when assessing whether a strategy should be pursued further, adapted or cancelled.

The agreed SBU-strategies and their objectives form the input for mid-range planning and for defining the results to be achieved in the coming year. In the functional concepts, the BSC-perspectives “processes” and “potentials” come to the fore. This is because operational planning must determine how the conditions for achieving the market and financial targets are to be created in the internal units.

This means that results to be achieved in the functional areas must also be defined as objectives. It should be possible to measure the success of implementation with the BSC. The processes are also to be specified in a verifiable form. The intention to “expand the customer base” does not help with work planning in the areas concerned, nor is it defined how much is to be achieved and how the results achieved are to be measured. The rules for agreeing on objectives are to be applied to both strategic and operational planning. It must therefore be specified which unit (cost center) is to acquire how many new customers, by when, which criteria are to be applied so that someone is counted as a new customer, and in which year what number of new customers is to be created.

In annual planning it is important to define the results to be achieved, i.e., measurable targets, in the planning of sales, revenue, production, projects, cost centers and investments, so that progress can be measured.

Implementation of the BSC thus requires that the ideas and rules of management by objectives are applied in all areas, that the quantity- and performance-related plan and actual data are available in the ERP (Enterprise Resource Management) and CRM (Customer Relationship Management) systems, and that decision-relevant plan, target and actual data on values and inventories are provided in Management Accounting.

Overall, the BSC runs parallel to the planning stages required in the management control system. Kaplan and Norton assume the same sequence and the same contents of the planning stages as described in this blog. Based on the corporate policy and strategic definitions, the measurable short- and medium-term objectives for market development are to be derived. To realize them the personnel and material prerequisites must be created in the functional areas. This is done in cost centers and projects. The BSC measures and assesses whether these results are being achieved on time and within budget by means of target to actual comparisons.

If the management control system is set up as outlined in this blog, the planning data required for the BSC will also be generated.

The next post will analyze whether the management control system can also provide the actual data required for evaluation.