Last Updated on March 12, 2024 by Lukas Rieder

Costing or Pricing 1

In management, the question often arises as to whether it is primarily the sales prices and the company’s own costs that determine the company’s profit, or the design of the product range and of the market presence. Should planning start with costing or pricing?

Mostly the market, i.e. the potential customers and the competitors, as well as the skills of a company’s salespersons make the price. However, only the excess of the net revenues over the costs incurred for them results in the company profit. The profit of individual products or individual customers can neither be determined on a cause-and-effect basis nor for a single year because the costs of the readiness to perform (fixed costs) cannot be charged to customers or products/services on a direct cause and effect relationship (see the post “Full product costs are always wrong!“).

Managers have to decide whether to add a new product or even a product group to their product range, to serve new sales territories or sales channels, or even to invest in new technologies. For such expansions often investments have to be made and new cost elements arise in order to generate additional sales and contribution margins.

First it is necessary to estimate sales volumes, sales prices and net revenues per product, because this pricing-oriented data creates the basis for planning and determining the necessary investments and costs. It is necessary to think from the market into the company. The following rough sequence emerges:

-

- Prepare ideas for new products or services.

- Analyze competing products or services and thus expected competitors.

- Estimate possible sales quantities and net prices in various market dimensions such as sales territories, sales channels, product groups.

- Plan the quantities and the net revenues per item, per sales territory and per sales channel.

- Estimate annual additional costs for marketing, advertising, sales promotion, customer service.

- Decide.

Only when estimated values for point 4. are available, it makes sense to plan the costs and investments necessary for the implementation.

To generate a plan-calculation Dynamic Capital Budgeting is the suitable instrument (see the post “Dynamic Capital Budgeting”). This is because it allows sales and net revenue estimates to be compared with cash outlays for new investments and expected costs, the payback period to be calculated and the present values to be discounted to the decision point. Existing contribution margin and cost/performance calculations can provide essential planning inputs, but they do not yet include the new products and submarkets. It is therefore advisable to first calculate the expected net sales and contribution margins in a separate table.

Offer leatherette presentation folders? (Costing or Pricing 1)

The management of Ringbook Ltd. is discussing the idea of adding high-quality presentation ring binders with imitation leather covers to the product range. These ring binders for presentation should help customers promote their own offers more successfully.

The leatherette folders are to be sold through the existing three sales channels (direct sales to companies, to retailers for resale and via online store). For the time being, sales are only planned in the home market (Switzerland).

Market assessment

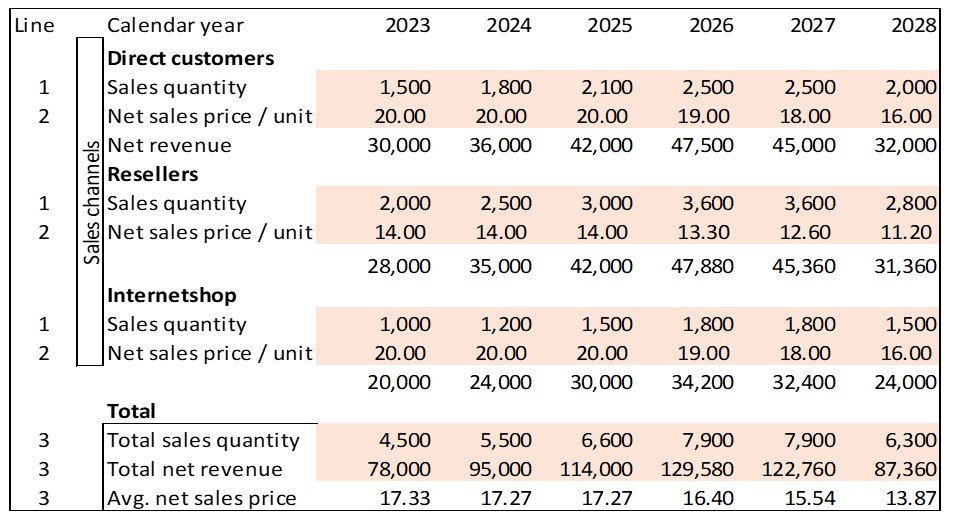

In an initial assessment, the sales management and the sales staff of Ringbook Ltd. agreed on the following potential net sales prices (after deduction of discounts of all kinds) and sales volumes for the Swiss home market:

The salespersons in the respective regions estimated the sales volumes of presentation folders that they believe can be realized (line 1). The assumed development of the planned sales quantities shows that they assumed that the life cycle curve of the product will reach its peak in the fifth year and that subsequently the sales volumes will decrease.

Ringbook Ltd. grants its customers various discounts on list prices and on order values. The total average discounts granted to date have already been taken into account in the net sales prices. This explains the different net sales prices per unit (lines 2).

From this, the net sales to be achieved with the intended presentation folders were calculated for the individual years per sales area. Lines 3 also show the estimated average selling prices per unit.

The inclusion of presentation folders in the product range is intended to help Ringbook Ltd. be included in the inner circle of potential suppliers of sales support aids for all potential customers. This should help to continuously improve the company’s own market position.

The table with the sales channel-related planned sales quantities and net revenues is thus an approach to quantify strategic intentions. It is the basis for comparing the planned net revenues with the expected costs and expenses. Only this comparison can show whether the expansion of the product range will also improve Ringbook Ltd.’s financial result.