Management Summary and Simulation Model

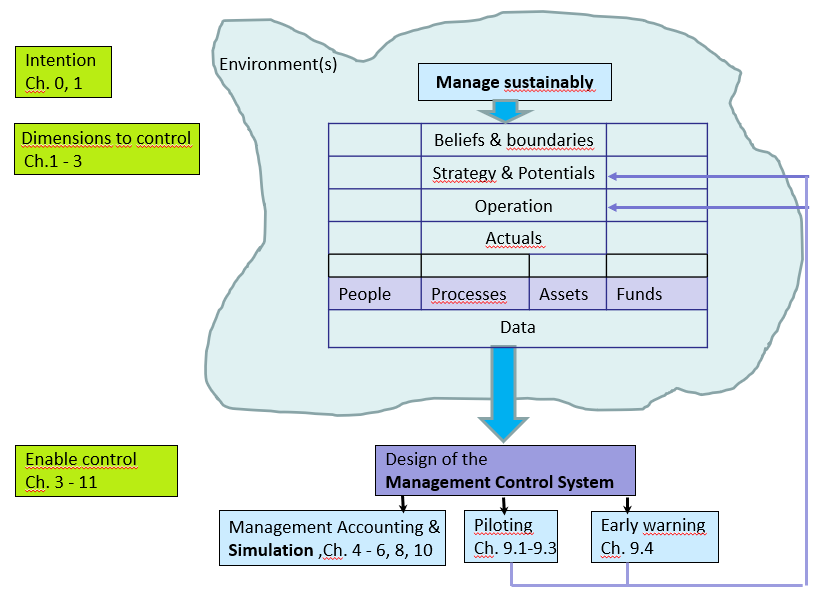

Management Control means successfully planning and controlling all dimensions of sustainable corporate management. This requires a management control system that incorporates all relevant dimensions of internal actions and external environments.

With early warning signals from the environment significant future developments and market opportunities are identified. Inside the company, piloting information is used for comprehensive multi-year planning, which helps to generate competitive advantages. Management accounting supports the realization of operational objectives and plans, which should lead to the achievement of results and to the development of the future potentials for success.

Management Control System = Management Accounting + Piloting + Early Warning

The book provides guidance on building an integrated planning and control system. The requirements are derived from holistic management models as well as from the practice of corporate management.

The included simulation model is built as a Resource Consumption Accounting (RCA) system. RCA incorporates marginal costing (GPK), contribution margin accounting and Activity Based Costing ABC. RCA enables every manager to plan and control those quantities and values for which he is directly responsible.

The simulation model serves three purposes:

1: Comprehension of all operational connections and their details with a concrete example. Integrated are among others: Sales planning, customers, procurement/inventories, production, multidimensional profitability analysis and, of course, aggregation up to the balance sheet.

2: Recognition of the effects on other areas when initial values are changed as well as tracking of the resulting consequences over 5 years up to the internal balance sheet.

3: Decisions to be made and calculations that can be automated are clearly separated. This creates the design template for building a company’s own planning and control system.

The model is a completely programmed Excel application (>500’000 cells). It is ready to use and requires only basic navigation skills in Excel.

Summary of the book “Management Control with Integrated Planning”

Many managers want a well-structured system for the holistic and coordinated planning and control of their companies and their parts. In designing such systems it is necessary to start with an organization’s purpose and core values so that individuals as leaders of their organizational units are able to understand the results to be achieved. Additionally, managers need to be able to directly control the input factors they are responsible for, and need to be accountable for the results achieved by those factors. This requires the formulation of the results to be achieved in a measurable, or at least a verifiable, form. Aggregation of these results to the overall organizational result should be possible, requiring the performance measures to be quantified in a similar manner.

The proposal presented here for the establishment of a comprehensive management control system is largely centered on discussion of performance and financial data. However, dysfunctional decision-making behavior that impedes the optimal implementation of the system also needs to be considered and addressed as far as possible.

It is shown how planning from the corporate purpose down to the individual aspects of a project (or a manufactured product, a customer, an employee, a supplier) becomes feasible and how the achieved results can be measured so that they become relevant for organizational control. Every manager, from the foreman up to top management, should recognize which data and parameters they need for planning and controlling their individual area of responsibility.

The designers of the necessary information system (above all controllers and IT specialists) recognize which planning and piloting figures are to be presented in the planning and control system so that system users can act independently.

The conceptualization of the presented system is multidimensional in order to achieve general validity and integrated applicability. It includes the following attributes:

-

- Hierarchical: From the CEO to the group leader

- Planning: From corporate policy and strategy to the individual process

- Content: From the corporate purpose to the production order

- Functional: From sales to production and R&D to support areas

- Comprehensive: From the single project to the exchange of services in corporate groups

- Behavioral: From reluctance to plan to actions to maintain its own hierarchical position.

- Time reference: From early-warning and piloting to yearly planning, actuals and forecast.

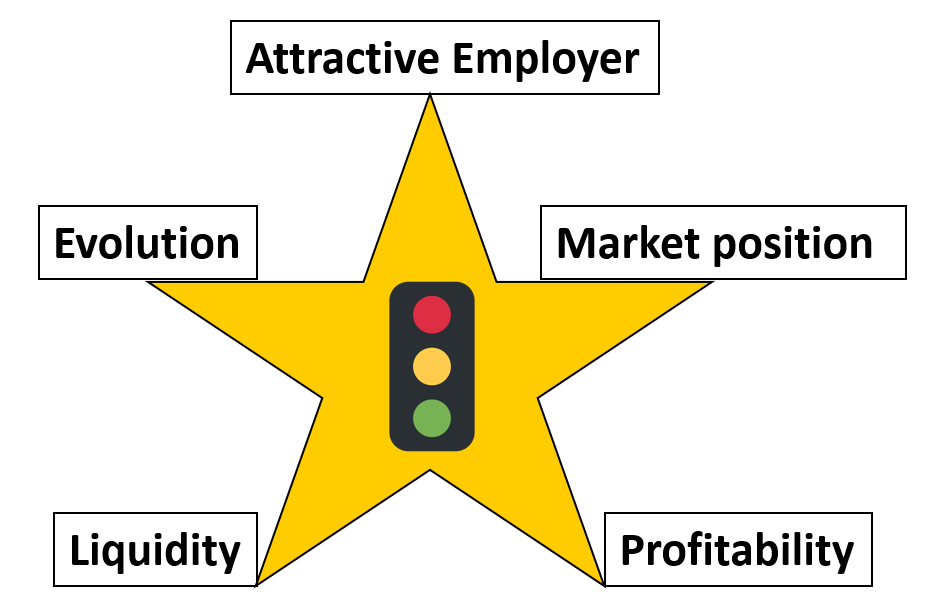

We use the term AMPLE to represent the five top performance controls of sustainable success, and graphically portray these controls as shown in the figure below. AMPLE provides orientation. To be and to remain successful in these areas requires many preliminary achievements that are hard to measure such as appropriate leadership behavior, creative ideas, process productivity and luck. These aspects are only partially addressed here; our focus is on measuring results achieved from utilization of the inputs.

To obtain decision-relevant parameters, top-down and bottom-up viewpoints are alternately utilized. This changing of perspective provides appropriate scope to the decision-making of the manager involved and ensures that the various aspects of corporate management are mapped in parallel. This process is known as the counter-current principle (see Glossary).

An objective is a result or state to be achieved. Objectives need to be formulated so that they are measurable and verifiable. Results should be able to be aggregated up to the whole organization, which automatically results in a focus on technical, performance-related and ultimately financial parameters.

A holistic understanding of the company, the application of fundamental management principles and the consistent application of structural and procedural concepts are prerequisites for integrated corporate management. Particularly relevant terms for system-design are developed in Chapters 1 and 2. In Chapters 2 and 3, based on AMPLE and findings from the explanation of integrated management models, the requirements for a comprehensive planning and control system are designed top-down. Chapters 4 to 6 deal with operational annual planning, the recording of achieved results and tactical management during the year.

Corporate policy, strategic and medium-term planning and control require instruments with a multi-year horizon and a link to annual performance. Suitable instruments – further based on the accompanying model – are dealt with in chapters 7 to 10.

Additional components of this book include the documentation of the accompanying simulation model as well as an extensive glossary. The simulation model is extensively integrated into the book and is a great resource which shows in detail how this methodology can be implemented in any organization.

Simulation Model

Part of the book “Management Control with Integrated Planning” is a comprehensive Excel simulation model. It serves as a step-by-step guide to demonstrate:

-

- The individual segment plans

- Their mutual dependencies

- The system-design requirements resulting from the management processes and the decisions to be taken

- The necessary links that must be established to arrive at the plan result

- The required databases for the recording of real results

- The presentation and interpretation of the individual as well as overall results in plan, target to actual comparison with the purpose to derive target-oriented corrective measures.