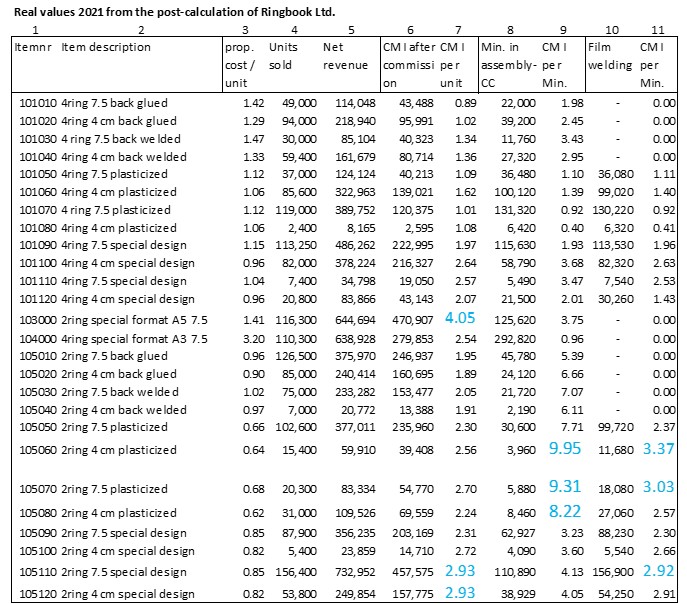

The table below shows how much contribution margin I per bottleneck unit is generated by the individual products of Ringbook Ltd. The data basis are the actual values of the year 2021 (sales volumes, realized net revenues, recalculated proportional manufacturing costs, actual employment in the assembly and foil welding cost centers). In each case, the best three items are marked in blue.

Column 7 shows that item 103000 achieves the largest contribution margin per unit (4.05). This is followed by articles 105110 and 105120. It is therefore worthwhile for the salespersons and for the company to concentrate primarily on these three products. 4.56 units of item 101010 must be sold to generate the same contribution margin for fixed cost coverage as one unit of 103000. The market potential of the standard item 101010 (first line) is naturally much greater than that of item 103000 (special A5 format with wide back). The sales staff of Ringbook Ltd. recognized this and therefore exploited the market potential of article 103000 better than the competition, with 116,300 units sold.

The dominating bottleneck

Final assembly of the ring binders takes place in cost center 250 (Assembly). Column 9 shows that the articles 105060, 105070, 105080 achieve the highest contribution margins per minute of assembly time. If assembly becomes a bottleneck due to machine failure or insufficient personnel, the articles mentioned are consequently to be produced first.

If the available output in the foil welding shop becomes a bottleneck, this only affects the foil-wrapped articles. Of these, articles 105060, 105070 and 105110 are to be produced first, as they achieve the highest CM I per minute of bottleneck utilization.

Since the material consumption for sheet steel and wire is more than twice as large for 4-ring binders as for 2-ring binders, in the event of a supply bottleneck for these raw materials, the achievable CM I per piece would have to be related to the individual material costs per piece (not shown here).

Prerequisites for bottleneck analyses are on the one hand, the existence of the bills of material and the routings of the products to be manufactured. On the other hand the split into proportional and fixed costs must be set up in cost center planning. This is because to make optimum use of the remaining capacity in a bottleneck, it must be known which articles generate how much CM I per dominant bottleneck unit. For this calculation, the split into proportional and fixed costs is necessary in the cost centers so that the proportional product- and manufacturing costs can be determined.

Throughput

Typically, order intake is the dominant bottleneck. Customer demand and the skills of the sales force determine net revenue and contribution margin. When internal bottlenecks occur, the aim is to keep throughput as high as possible until they are eliminated. This would argue for selling and manufacturing primarily those products that make the least use of the bottleneck. However, the numerical example above showed that from the overall perspective of the company, contribution margin I must be maximized in order to cover the fixed costs and the target profit.

Therefore, it is important to sell first those products or services that achieve the highest CM I per bottleneck unit.

Inventory levels are not relevant to the decision-making process in terms of throughput. This is because the dominant bottleneck area must be continuously supplied with the raw materials and semi-finished products needed to operate at full capacity at all times. When and how much of an article is to be purchased is determined by the replenishment lead times, the delivery capabilities of the suppliers and their price conditions. In addition, there are safety stocks so that the cost centers can continue to produce if delivery is delayed for other reasons. Many manufacturing companies therefore try to agree “just-in-time” delivery with suppliers. This way, they oblige the suppliers to stock enough units in their own company.

Various reasons can lead to the fact that products and services manufactured or refined in-house cannot be delivered according to customer requirements, i.e. in line with incoming orders.

The possible causes are manifold:

Insufficient inventory of finished or semi-finished products

Lack of raw materials or late deliveries from suppliers

Energy or other operating material deficiencies

Failure of machines or tools

Insufficient personnel capacities in production cost centers

Delayed final quality inspections of manufactured items

Insufficient production capacities of certain facilities

In such situations, it is important to identify the respective bottlenecks and to master them in such a way that the available capacities are used optimally until the bottleneck is eliminated. This optimal utilization occurs when the maximum possible contribution margin I is generated, taking into account the dominant bottleneck in each case. Because, as has been shown several times in this blog, the contribution margins generated are used to cover fixed costs and profit.

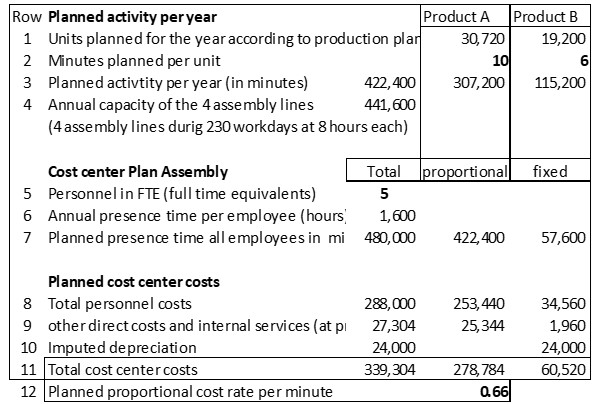

Cost center planning

In the example company Ringbook Ltd. the sleeves and closing mechanisms are joined together to ring binders ready for sale in the assembly cost center. For this purpose 4 parallel assembly lines are available. Each of these lines is in operation for 8 hours per working day. With 230 annual working days, the capacity of each line is 230 * 8 * 60 minutes = 110,400 minutes. Together all four assembly lines have an annual capacity of 441,600 minutes.

Production management planned an annual activity of the assembly area of 422’400 minutes (see lines 1 – 3). The capacity of 441,600 minutes should therefore be sufficient for the planned production. For each piece of ring binder produced, an employee in the assembly department works 1 minute. 57,600 minutes are planned per year for organization, cleaning, maintenance and training (lines 6 and 7). In total, the presence time of the five employees (including cost center managers) amounts to 480,000 minutes. After taking into account the other direct costs, the costs directly caused by the products amount to 278,784 in line 11 in the “proportional” column and the proportional planned cost rate of 0.66 per minute in line 12.

Costcenter plan “Assembly”

Product costing and contribution margins

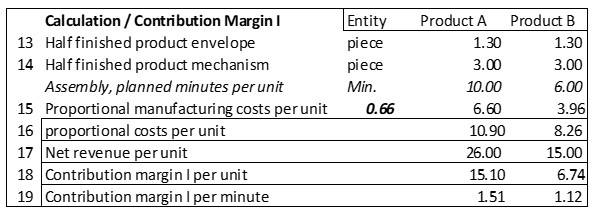

In lines 13 – 19, the product costing and contribution margin calculation can be traced. Product A requires 10 minutes per piece in the assembly line, product B 6 minutes. Together with the costs for the envelope and for the binder mechanism, the proportional costs per unit result in line 16. In line 18, the contribution margins per unit are calculated.

Contribution margin per unit

Machine breakdown in assembly

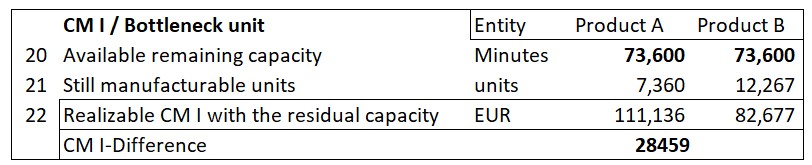

One of the four assembly lines suffers a machine breakdown. The supplier reports that four months !! will pass until the necessary spare parts will be delivered and the plant will be ready for operation again. As a result, one third of the capacity of one of the four lines is missing, namely 36,800 machine minutes (cf. line 4: 441,600 / 4 / 12 x 4). These are no longer available for assembly.

The production manager wants to reduce the production of product A because each unit of A requires 10 minutes of production time, whereas for product B it is only 6 minutes per unit (line 2). The sales manager replies in the management meeting that the contribution margins of the products must be considered before the production program is determined. Who is on the right track?

Line 19 gives the answer. Product A generates a CM I per piece of 15.10. Per minute of bottleneck usage (cost center assembly) this is 1.51. Product B uses the bottleneck less, but because of the lower sales price “only” generates a CM I of 1.12 per minute.

CMI per bottleneck unit

If the remaining capacity of 73,600 minutes (line 20) were used exclusively for product A, a CM I of 111,136 could be generated, while concentrating on product B would generate 82,677 (line 22). This is, of course, a hypothetical calculation, since what has to be produced is what the customers buy. However, the difference of 28,459 CM I between the two products shows that concentrating on the products that are stronger in terms of the bottleneck leads to a higher total CM I and thus to a better company result.

This example intends to show that in operational management it is necessary to analyze in each case how a bottleneck affects the overall result, e.g. earnings before interest and taxes (EBIT). For this purpose, the CM I per bottleneck unit must be calculated. Bottlenecks can be raw materials that are difficult to procure, insufficient service availability from suppliers, own personnel capacities or the availability of own equipment.

If the activity level decreases, but the personnel cannot be used in other cost centers or cannot be committed to a lower degree of employment, the fixed costs, resp. the spending variances of the considered cost center increase. To avoid this is the task of the cost center manager concerned.

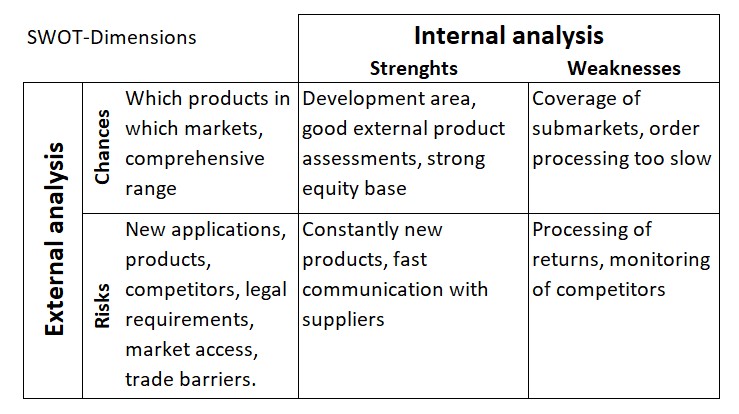

SWOT analysis is intended to produce a structured representation of the strengths and weaknesses of the organization under consideration and to contrast these with the opportunities and threats in the four environmental spheres (cf. the post “Environmental Changes are Crucial for Management Control“).

The purpose of the opportunities/risks and strengths/weaknesses assessment is to,

create the basis for strategic planning and

define the success potentials necessary for their realization.

A SWOT analysis is primarily prepared by the top management of an organization. They determine whereto the company / organization should develop and assess whether the targeted development will be feasible in the medium-term time horizon. The decisions derived from a SWOT analysis form the planning template for the strategic and operational planning executives.

Subordinate management levels should be able to derive which services and products the company should use to achieve strong positions in nominated markets and which results should be achieved in the process (corporate policy determinations).

The assessment and documentation of external opportunities and risks and the evaluation of the company’s own strengths and weaknesses form the input for strategic and medium-term planning.

Analysis of the environment and of the own position

The widely known SWOT matrix shows the initial questions of the analysis:

Business environment: In which environmental areas are opportunities for new products and services suspected and which threats could prevent success?

Own development direction: In which product/market combinations does the company see its strengths for expanding its market position, and which of its own weaknesses could prevent success?

SWOT Analysis

The above questions on opportunities and risks are examples. The same applies to the assessments of the strengths and weaknesses of the own company.

If a company’s management creates its own SWOT analysis and records its findings in the matrix, the subsequent management levels can align their strategic plans and, above all, the development of future success potentials accordingly.

How the strategic and medium-term plans for the entire company are derived from the SWOT analysis is the subject of the following posts:

CZSG Controller Zentrum St. Gallen/Switzerland introduced many decision-relevant planning and control systems mainly in German speaking countries. The basis was always “Grenzplankostenrechnung GPK” and the further developments arising from it. The applied management accounting principles correspond almost 100% to the recommendations for the design of “Resource Consumption Accounting RCA” according to Larry R. White and of the Profitability Analytics Center of Excellence PACE.

Who decides what?

Many chief financial officers and cost accountants see the purpose of management accounting primarily as presenting an organization’s financial results in accordance with the requirements of local accounting laws, IFRS and USGAAP, local tax laws and regulations for setting transfer prices between related companies, and other regulations.

In our eyes the purpose of management accounting is first and foremost to provide decision support for managers at all hierarchical levels. After all, they are responsible for the results to their superiors. The focus is on management support, not on external reporting.

Customers decide whether they want to place an order and at what price. In this way, they also indirectly decide the proportional manufacturing costs of the products or services to be sold and manufactured. Managers at all levels decide how the necessary offers are to be made and what personnel and machine capacities will be required to process the orders won and, in doing so, to achieve a profit with the company in line with the complete market.

In strategic and operational planning, managers at all levels must define activities, quantities and capacities. Consequently, consumption according to bills of materials and work plans as well as activity-based cost center budgets are required for planning and subsequent control. Only when these quantities and activities are known can they be valued in monetary terms. A management accounting system that is suitable for decision-making must therefore provide those quantities, activities and valuations which a responsible manager can control himself and thus take responsibility for. This also requires that the manager can always compare the planned values with the actual values of his area.

This starting position applies to manufacturing companies, service providers, hospitals, retailers as well as banks and government institutions.

No financial accounting system can provide this data, as it only represents values. Valuation regulations from tax law, from accounting standards (US GAAP, IFRS) or from specifications for the determination of international transfer prices are also irrelevant in accounting for management, because cost center managers, product managers and salespersons cannot change these values themselves.

Responsibilities of different managers

(usual period of consideration is one month).

Since managers are responsible for achieving their objectives, it is useful to list their responsibilities.

Production manager:

Timely processing of dispatched production orders

Ensuring stock receipts of semi-finished and finished products (valued at proportional standard production costs)

Adherence to target consumption rates for materials and cost center activities in accordance with the precalculation of released production orders, valuation of consumption at planned purchase prices and proportional planned cost rates

Compliance with the planned costs of its own cost center(s)

Notify other areas when capacity constraints become apparent.

Cost Center Manager:

On-time completion of manufactured work

Adherence to the precalculated times in the production orders to be processed

Adherence to target costs (flexible budget) of own cost center, taking into account precalculated times and work performed.

Sales Manager:

Achievement of planned net revenues per period (invoiced).

Compliance with the planned costs of his own cost center(s)

Meeting the agreed delivery dates to the customers.

Purchasing Manager:

Procurement and on-time availability of all goods and services to be purchased.

Determination of planned prices (standard prices) for raw and auxiliary materials as well as services to be purchased (on this basis the standard cost calculations are prepared)

Informing sales and production in the event of major variances between actual and planned purchase prices.

Who is responsible for depreciation?

The manager in whose cost center the asset is located,

the managers who determined the planned useful life of an asset on the occasion of the investment decision,

the financial manager or the controller who determines the depreciation method (preferably fixed depreciation from the replacement value of an equally efficient asset)

Depreciation is mainly a period cost, since most assets do not need to be replaced because they no longer function, but because they are technologically obsolete.

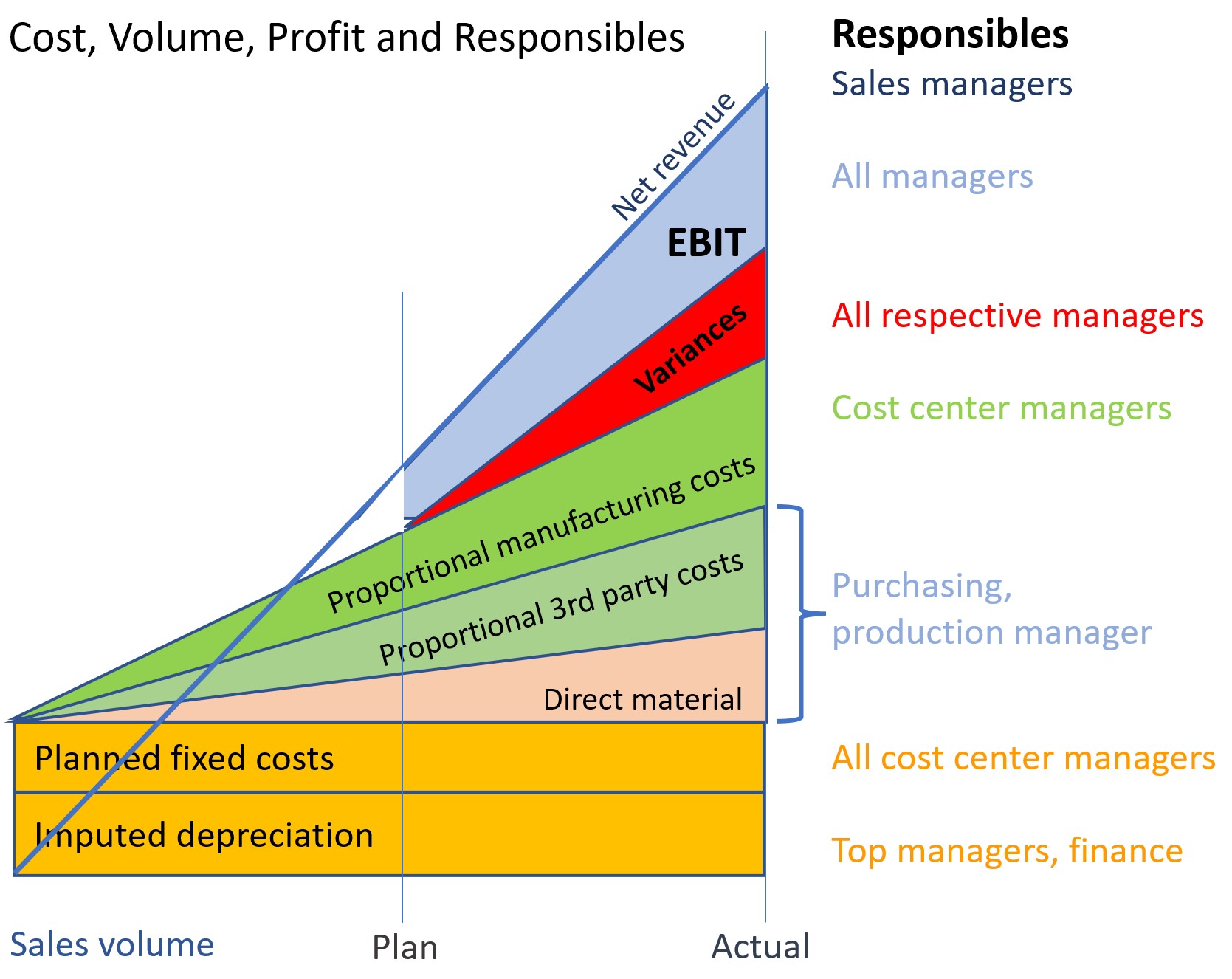

In the stratified presentation of the origin of results and profit, the contribution of the individual responsibles and their employees becomes apparent:

Decision-Making, Responsibility and Causality

Who is responsible for idle capacity?

The managers who bought too large a plant,

the salespeople who sold too little

possibly cost center managers, if they do not point out idle capacity to their colleagues.

From this it can be deduced that it makes little sense to allocate costs of idle capacity (especially personnel and depreciation costs) to cost centers or product groups. As mentioned, imputed depreciation and personnel costs are charged to cost centers because they are observed there.

Strong and weak causalities

In our opinion, a strong causality is given if the consumption of an input good, e.g. the output of a cost center or an employee, is directly caused by the storeable or saleable product. This is the case if a routing or/and a bill of materials can be created for the product or the service unit performed. In Grenzplankostenrechnung GPK, therefore, only proportional costs are charged to products or services, and the remaining fixed costs are transferred to stepwise contribution accounting. This is because fixed costs can only be changed by management decisions, such as firing an employee or purchasing a machine.

Weakcausalities do not show a direct dependency between output and input.

Example 1: Because the headcount has increased, the human resources department needs an additional employee for everyday personnel support. There is no rule how many employees one person in the personnel department can supervise. It is a management decision whether to hire the person or not. The costs directly attributable to a manufactured product do not change as a result of the increase in staffing levels, since no changes are required in either the bills of materials or the routings. But the fixed costs of the company increase.

Example 2: A company fills gas cylinders and delivers them to customers by trucks (see the case study “Le Petomane Gas in the PACE homepage“). Delivering to a remote customer requires an additional hour of travel time, resulting in corresponding fuel and labor costs. These could be saved if the customer is no longer served. On the other hand, the net sales minus the proportional costs for the delivered gas cylinders, i.e. the contribution margins I of this customer would be eliminated. This results in:

+ omitted transport costs – omitted contribution margins.

The proportional product costs per filled gas cylinder in the finished goods warehouse can be clearly determined since material consumption and work schedule for filling are defined in the technical bases (strong causality).

Example 3: Most companies have a central IT cost center for the implementation, operation and maintenance of applications and data. The resulting data and evaluations are used (to varying degrees) by many cost centers. In cost accounting, therefore, a search is often made for cause-effect chains by means of which the IT costs could be charged to the receiving cost centers. Mostly this search is unsuccessful because both the data sets and the applications are used by a wide variety of cost centers (very weak causality).

Nevertheless, many financial managers and cost accountants try to allocate the fixed costs of the IT department (including depreciation) to the various cost centers and from there to the manufactured products by means of one or more allocation keys. After all, according to the widespread opinion that each product must bear its share of the total fixed costs. However, the IT manager plans and controls the costs of the IT department and is consequently also responsible for them to the management. There is no need to allocate costs to individual cost centers and products. The contribution margin from sales must be sufficient to cover all fixed costs plus the target profit.

Insight:

In Grenzplankostenrechnung GPK, only proportional costs are charged to manufactured products because they were directly caused by the products (only strong causalities). Therefore, in management-oriented cost and revenue accounting, inventories should also be valued only at proportional (standard proportional product costs). This is because fixed costs are period costs and, as such, should be shown as blocks in the contribution margin accounting. They are to be controlled in the cost centers.

To put it even more clearly:

In GPK and in Resource Consumption Accounting RCA, fixed cost allocations have no place because these allocations are an attempt to delegate cost responsibility to units that have no direct possibility of influencing the costs at the point of origin.

Of course, it makes sense to include fixed costs in pricing for individual customers. However, in our view, this is activity-based pricing, not costing. Therefore, considerations about setting offer prices and conditions should be made outside the management accounting system, especially in the sales organization.

If in the Costing Levels Continuum Maturity Model from Gary Cokins the levels 11 and 12 are to be reached, all allocations of fixed costs must be eliminated, because otherwise no useful simulations are possible.

The term “Internal Tasks” stands for all work to be performed in a company that is not directly caused by the units produced or by the activity of the receiving cost center. Internal tasks are only indirectly related to the products and services produced or sold. For better distinction we always write the term in our blogs with a capital “I”.

Examples of Internal tasks:

Management, planning and control work in all areas

Work of all sales-oriented cost centers

The entire production planning and control as well as work preparation

Work of personnel administration, payroll accounting and the time spent on training and further education

Work of procurement, warehousing, forwarding

Development and operation of the entire information technology as far as its services are not directly caused by orders from individual cost centers or customers.

Work to keep buildings, company premises, installations and machines ready for operation

Administrative work to comply with legal requirements.

All these Internal tasks have in common that they are rendered to keep the whole organization ready to perform. How much work capacity is built up and provided by employees or plant capacity is decided by managers as part of strategic and operational planning.

Planning hourly requirements for internal tasks

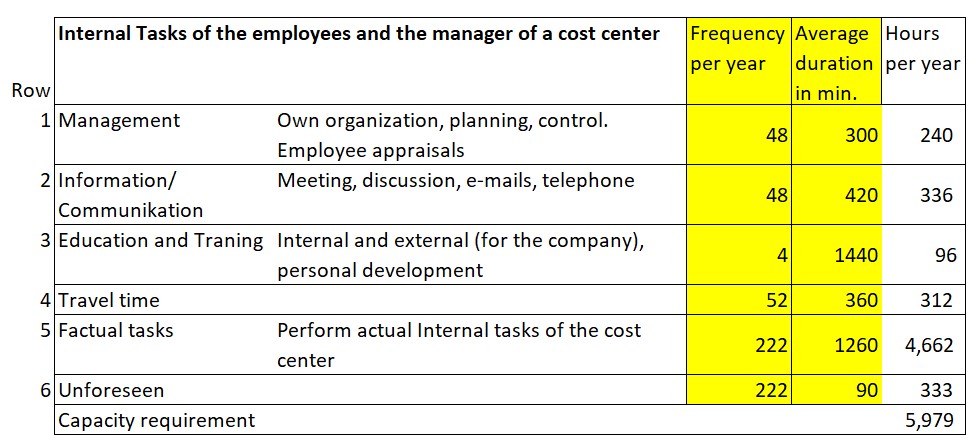

More than 50% of total personnel costs are incurred for Internal tasks in many industrial and service companies today. Therefore, the annual hourly requirements for these tasks must be planned and recorded in each cost center.

The difficulty lies in creating reliable capacity requirement plans for all Internal tasks. On the one hand, this is due to the fact that people in these areas perform a wide variety of tasks more or less in parallel. On the other hand, only a few companies record time consumption for Internal tasks. This makes it difficult to plan requirements.

To get a better grip on capacities and the cost block for Internal tasks, we recommend since years that the worked hours for Internal tasks should also be recorded by types of work. The presence time of a person can be measured quite easily using time recording devices but many managers are not even required to perform this recording for themselves. But just from recording the presence time it is not possible to evaluate for which task type how much time was spent.

We made the experience that already the planning of the task types in the internal areas generates important insights for capacity planning. For this purpose, the Internal tasks are divided into six groups, which occur in almost every cost center:

Capacity requirements for Internal Tasks

For the factual tasks (Row 5) subgroups can be created in individual cost centers as needed. In the sales-related functions for example:

Addressing potential customers

Support of existing customers, preparation of offers

Capacity requirement for contract negotiation.

In the human resources department subgroups could be:

Recruitment and selection of personnel, payroll and social security

personnel and sickness care

Documentation of the potentials of managerial and professional staff.

Planning at this level of detail brings benefits to the whole company. Since employees are usually reluctant to record the time spent for different Internal tasks, a user-friendly and thus largely automated recording application must be set up.

Thanks to the lean production movement impressive improvements were already achieved in the area of directly product-related services and production management. Now it is time to apply the findings to Lean Administration as well (see the corresponding posts in the Lean Management area of this blog).

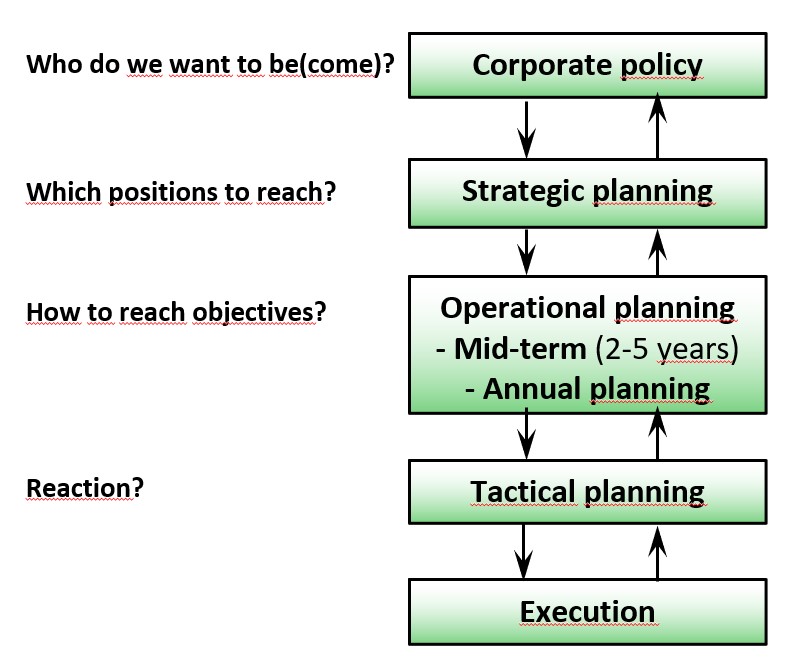

Planning and controlling from top to bottom or vice versa?

Countercurrent Principle

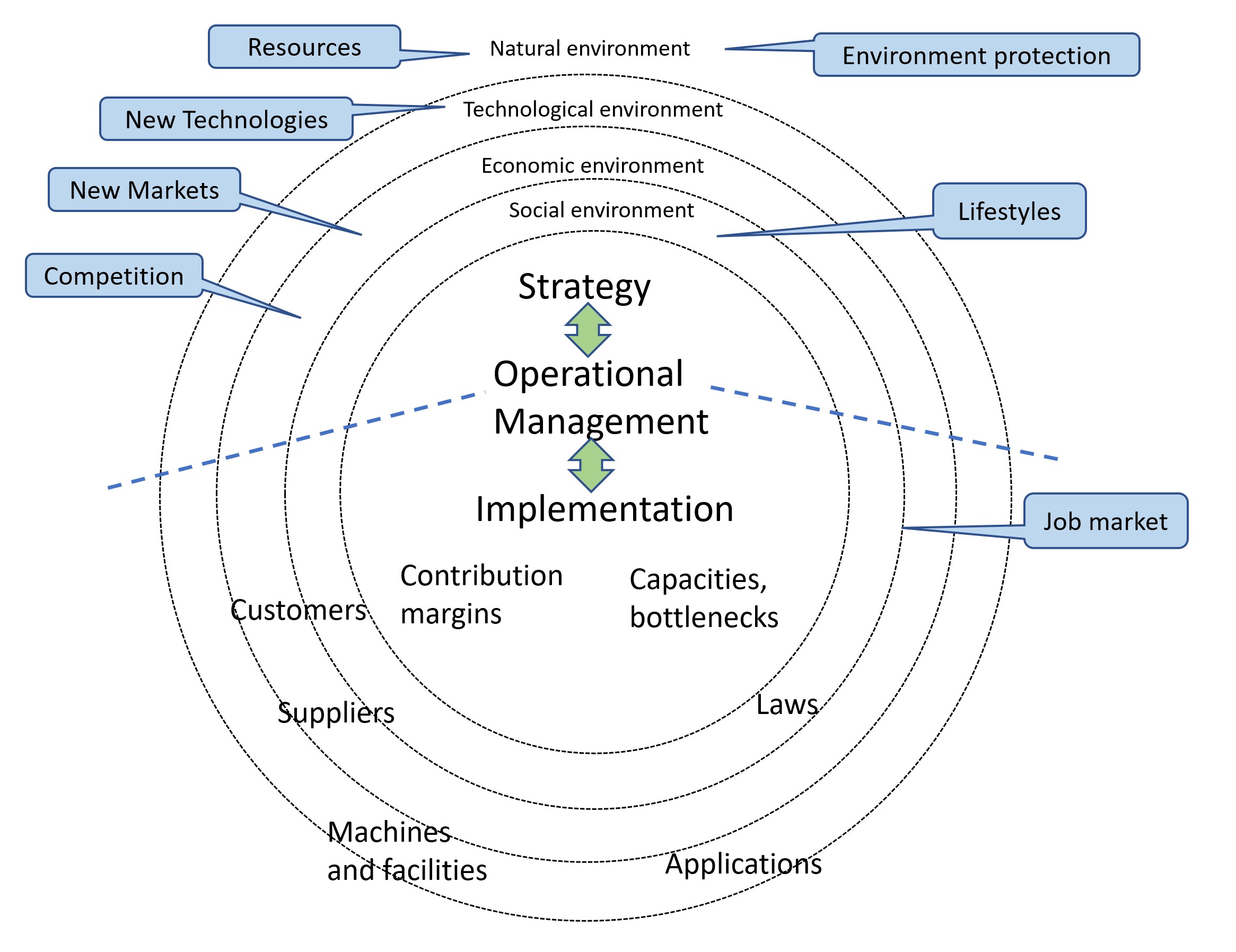

Anyone involved in the design of sustainable management systems automatically ends up with the question of whether to plan and control top-down or bottom-up. The answer is to proceed according to the countercurrent principle.

The post “The Main Questions of each Planning stage” shows that it is first necessary to answer what an organization wants to be or to become before implementation can be tackled. This determination is made by a small group of people, usually the owners. In corporate policy, they record their intentions regarding the markets to be served and the products or services to be provided for them. This is top-down leadership.

In strategic plans, the managers responsible for implementation specify which products and services they want to use to realize the corporate policy intentions in which markets (top-down). Before they can define the strategy, they have to make sure that the operating units of the company will be able to produce and sell the required products and services on time and in line with the market. To do this, they need feedback from the managers who will be responsible for implementation. The downstream managers assess from their operational perspective whether they have the personnel, factual, time and financial scope to implement the strategy operationally. This countercurrent assessment can lead to the adjustment of strategies. If this feedback is omitted or negated in decision making, there is a great risk that the strategies will cost more than they can deliver.

Countercurrent principle

In operational planning and control, the feedforward and feedback loop is repeated. The available personnel, the existing facilities and the current processes must be able to handle the projects required for strategy implementation in a proper and timely manner, to bring in the necessary sales at net sales revenues in line with objectives and to keep within the planned fixed costs.

Reporting must be bottom-up because actual data on sales, production, personnel development, project progress and the like are prerequisites for determining the target achievement of the objectives in a period under review.

These reports cannot be neglected in the next planning round if realistic objectives are to be agreed. The counterflow of data and assessments of real implementation thus forms the indispensable bottom-up input for agreeing on the next objectives.

Another argument in favor of applying the countercurrent principle is that in strategic management, other, usually more uncertain data from the environmental spheres (cf. the post “Environmental Changes are Crucial for Management Control”), are collected and evaluated more than in operational planning and control. In addition, the time horizons are different. In the upper part of the figure below, the focus is on the internal success potentials required for strategy implementation. In the lower part, an assessment is made of how successful the implementation was and how the development of future success potentials went. This assessment may lead to the need to adjust the objectives for the next periods.

Considering the development of the environment in the countercurrent principle

Conclusion: Planning top-down is a prerequisite for determining an organization’s future potential and realizing it on schedule. However, operational results, bottlenecks in manufacturing, delays in research and development, and customer and supplier bottlenecks or a dried-up labor market can lead to changes in operational and strategic goals. Feedback loops must therefore be built into the planning process. Committed employees often contributed ideas that led to the realignment of a company.

Agile team management is based on the assumption that teams act on their own responsibility. However, this does not mean that they can change their mission without considering the higher-level objectives (see “Prerequisites for Agile Team Management“).

A company can rarely pass on supplier price increases in full to its customers. Managing inflation internally is a must. This is because the company’s existing customers will, in their own interest, try to buy cheaper from other suppliers, consume less, use other input materials or even withdraw their own offerings from the market, because they are no longer profitable due to price increases. Potential new customers will also compare offered prices and services and order where they feel they get the most for their money.

A bidding company must therefore maintain its own profitability despite inflation so that it can continue to invest in its own future. Professor Simon calls this profit defense (p. 56 in the book Beating Inflation). In terms of planning and control, profit “should be included in the calculation from the outset like a cost variable to be covered (ibid., p. 52).” This requires the continuous increase of effectiveness and efficiency of one’s own actions. (Definitions in the glossary)

Effectivity = doing the right things

Efficiency = doing the right things right.

Therefore, all cost centers must find, decide on and implement measures that are suitable for achieving profitability in line with the market (see “Profit in Line with the Market “).

Cost reduction measures for functional areas

The ROI-tree from the post “ROI and Inflation” helps to generate ideas to increase profits, to evaluate these ideas from a financial point of view and finally to measure their implementation success. Exemplary starting points are structured below according to functional areas:

Managing Inflation internally

Sales, prices, conditions:

Announce and justify price increases quickly, even if customers temporarily switch to competitors (get ahead of the “cost wave” with price adjustments).

Increase prices in several steps to discourage customers from switching.

Do not give discounts at the time of ordering but pay refunds when a predetermined purchase volume is reached (sales model).

Fix terms of payment without cash discounts and accelerate the dunning process in parallel (cash discounts directly reduce profits).

Develop new pricing models, e.g. pay per use or pay per period (applies especially to products or services with low proportional manufacturing costs).

If the product or service is superior to competing offers, customers will buy at even higher prices.

Marketing, sales, distribution:

Care for existing customers according to ABC-analysis (A and B customers generate higher absolute contributions and should consequently be looked after more intensively).

Continuous procurement of new leads (addresses of potential new customers) and prompt contacting.

Largely digital customer engagement to reduce customer visits (less travel).

Analysis of contribution margin development after trade shows and exhibitions.

Fix advertising contributions to reselling customers as a share of your contribution margin and grant them only after the sales have been achieved.

Free delivery of a part of the order quantity often reduces the customer contribution margin less than direct discount percentages from the sales price, because only the proportional costs reduce the contribution margin.

Continuous monitoring of competitors’ prices, assortments and sales development to locate opportunities for new offers.

Completely automated dunning system to reduce days sales outstanding.

Manufacturing processes / production planning and control:

Larger production batches reduce proportional manufacturing costs per unit, as setup times are incurred only once per batch. It is worthwhile to regularly reconcile order intake with inventory levels and the size of production orders.

Train employees to master several processes and thus have less idle time.

Automate process steps. In times of inflation, it is often easier to obtain funds for investment, albeit at higher interest rates.

Continuously check whether suppliers offer certain semi-finished products cheaper than you can produce them yourself (in- or outsourcing based on proportional manufacturing costs plus direct fixed costs of your own process).

Introduce computer-controlled processing steps and thus reduce manpower requirements.

Digitalization of planning and control of production orders as well as production data acquisition.

Reduce scrap.

Purchasing and inventory:

Consumption scheduling per purchased item based on planned consumption of production and sales in order to achieve more favorable framework-agreements with suppliers.

Regular comparisons of purchase prices of potential suppliers. Have a substitute supplier ready for each procurement item.

Immediate information of the sales department and other affected cost centers in case of imminent price changes of important articles or services to be procured.

Report purchase price variances from budgeted purchase prices on a monthly basis to estimate the impact on product and services to be sold in subsequent stages.

Research and development:

Find cheaper or more suitable input materials.

Reduce process turnaround time for customer-specific developments as quick responses build customer confidence.

Regular assessment of project progress with go/no go decision ends stagnant projects earlier and frees up research capacity.

Internal service areas:

Continually re-evaluate out- or insourcing (what do we maintain and repair ourselves, what do we outsource?).

Outsource maintenance and cleaning and reduce cadence if they are not a prerequisite for operational readiness (make fixed costs more controllable).

Do not charge fixed costs to recipients in internal activity allocation. The service provider is responsible for its own fixed costs.

Controller:

Fast execution of the planning process and prompt internal reporting are becoming increasingly important because inflation affects the procurement side quicker than the receipt of payments.

At low value added, cost management is concentrated on the purchasing side because purchase prices change quickly and strongly. At high value added, the focus is primarily on personnel costs. Inflation tends to lead to job cuts.

Introduce cost splitting into proportional and fixed costs both in planning and in target to actual comparisons.

Enable computer simulation of cost and revenue developments so that changes in volumes, prices and costs can be estimated in advance.

Apply dynamic investment calculations so that the effect of inflation on present values becomes apparent.

Management processes:

Determine responsibilities of individual management positions so that adherence to qualities, quantities, deadlines, and results can be determined.

Introduce company-wide Management by Objectives and regularly measure and assess the achievement of objectives by individual employees.

Introduce shop floor data collection also in administrative areas to continuously reduce time consumption in these areas.

Fighting inflation internally is the task of managers at all levels of the hierarchy. If they do not manage to make the total value-added costs grow slower than net revenues, the company will lack the profits to invest in the future and will disappear from the market over time.

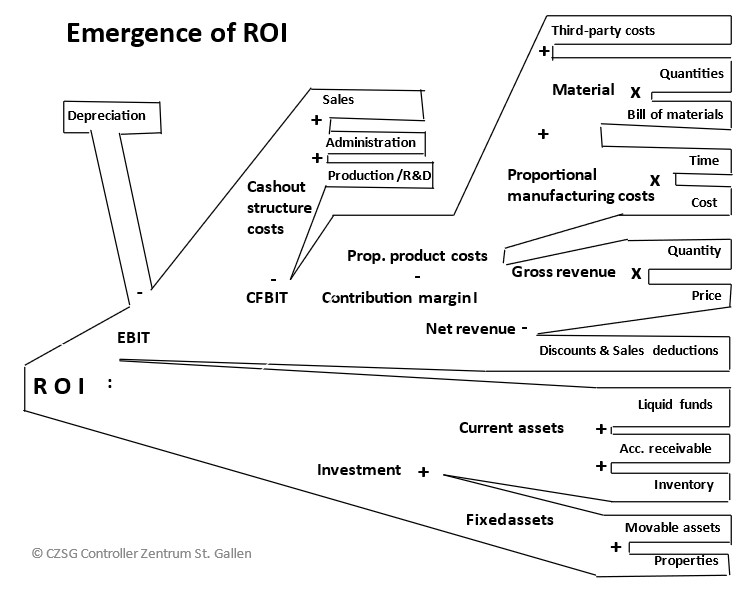

Profit before deduction of taxes and interest (EBIT) : invested assets.

EBIT (100) / Balance sheet total (1,000) = ROI (10%)

The financing structure, i.e. the shares of debt and equity on the balance sheet total, is therefore not taken into account. This enables the profitability comparison between different companies even if they have different financing structures.

If the revenue and cost sides of a company are broken down into their main components, it is possible to see which items affect ROI and to what extent. We call this representation the “ROI tree”.

ROI and Inflation

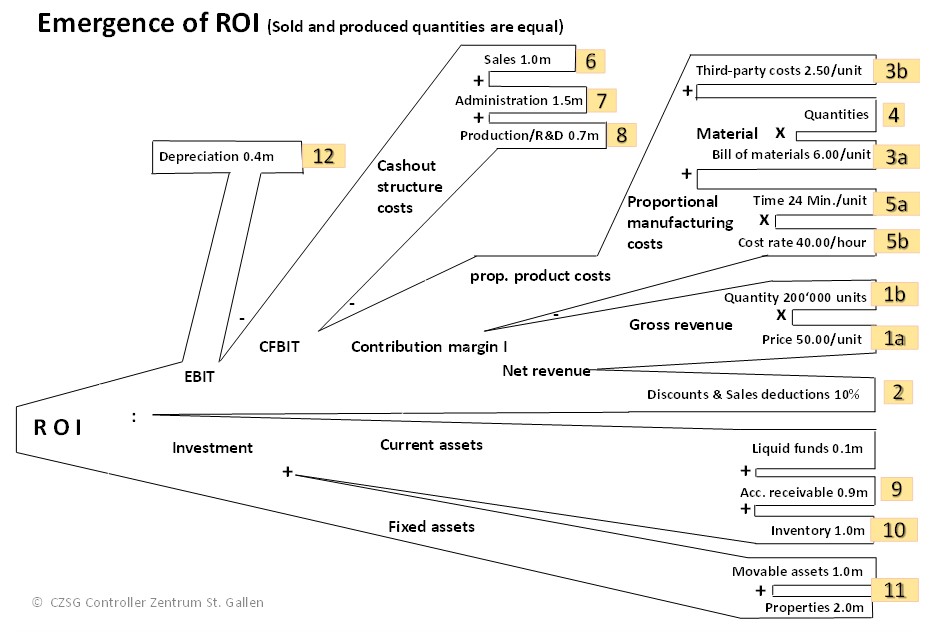

In the example, 200,000 units were sold at a gross price of 50.- per unit. This corresponded to the gross revenue of 10.0 million. 10% discounts and other sales deductions were deducted from this, resulting in net revenue of 9.0 million (1a, 1b, 2).

The direct material and unit-related external service costs amounted to 8.50 per unit (3a, 3b, 4). Manufacturing consumed 24 minutes per piece, which at the rate of 40.00 per hour resulted in a proportional manufacturing cost of 16.00 per piece. Multiplied by the production quantity of 200,000 pieces, the proportional production costs were 4.9 million (5a,5b).

This resulted in a contribution margin I (CM I) of 4.1 million.

CM I was used to cover the fixed cost center costs of the functional areas (6, 7, 8), which resulted in a cash flow before deduction of interest and taxes of 0.9 million. After deducting imputed depreciation and amortization of 0.4 million, the profit before interest and taxes (EBIT) was 0.5 million.

Dividing the EBIT of 0.5 million by the assets invested in the period of 5.0 million (9, 10, 11) gives the ROI of 10% in the year under review.

Effects of inflation

If the suppliers of materials and external services increase prices by 5%, this results in a cost increase of 0.085 million for the company. The graph shows that this amount has a direct impact on EBIT and thus also on ROI. See also the post “Purchase Price Variances are topical again”).

In the same way, price increases for auxiliary materials and purchased services have an impact on the cost centers. This affects the production centers (5a, 5b) as well as the cost centers of the other functional areas (6, 7, 8).

If machines, buildings, equipment and intangible goods become more expensive, the imputed depreciation increases as a consequence, which again lowers EBIT and thus ROI (12).

Another consequence of inflation is that employees lose purchasing power. They will demand – somewhat delayed – higher wages (5b, 6, 7, 8).

On the left side of the balance sheet, inflation also leads to higher invested assets.

If inventory levels remain the same, the average value of the stock will rise (10).

Banks will raise interest rates on loans, which will reduce pre-tax profits. In the end, business owners (partners, shareholders) will also demand higher dividends because the purchasing power of their dividend income will also decrease.

Conclusion: Inflation is a vicious circle that must be broken by all means. In the private sphere, renunciation must be practiced in order to cope with disposable income and assets. In the corporate sector, attempts must be made to push through price increases. In doing so, there is always the risk that customers will jump to other suppliers, resulting in a drop in sales. Even more important is to strive to improve efficiency in all areas, i.e. to break the vicious circle through more cost-effective processes and structures.

Starting points for improving efficiency are the subject of the next post.

“Beating Inflation” is the title of the book by Prof. Dr. Hermann Simon, the “old master” in price management and profit control, published in 2022. This publication deals with the demands that the currently again rampant inflation places on corporate management. Many of his statements are also essential inputs for the design of a comprehensive management control system and thus for the sustainable success of a company. In this and in the next two posts of this blog, his insights will be combined with the design of the comprehensive planning and control system of a company.

After a period of about 40 years with hardly any significant inflation rates, Europe and the entire English-speaking world are affected by massive price increases as a result of the COVID pandemic and war-related events. Many managers are experiencing inflation intensely for the first time and need to understand how to plan and act in such a situation in order for their companies to survive successfully.

How price increases propagate

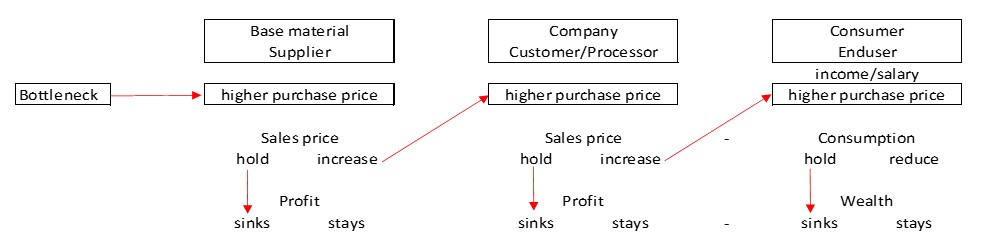

Generalizing, price increases are the result of bottleneck situations. Bottlenecks can arise in various areas when demand is greater than available supply. Insufficient supply capacity is often due to:

Raw material availability in the required qualities too low

Lack of transport capacity or transport containers

Political/legal supply restrictions

Inability to comply (yet) with regulations on manufacturing processes or guarantees of origin

Insufficient personnel capacity for processing and handling

Too little equipment available for manufacturing or insufficient manufacturing capacity

Too much capital investment ris equired for manufacturing.

Such bottlenecks lead to cost increases for suppliers of material and services. They try to pass on the cost increases to their customers in the form of higher net selling prices. If this succeeds, the purchase prices for the (further) processing companies rise. These price increases must in turn be passed on to the next (production) level. If a company cannot successfully pass on its higher costs, it will sooner or later incur losses, become insolvent and go bankrupt.

Beating Inflation

At the end of this chain are the end customers, usually private individuals. If purchase prices rise for them, they consider which of the available products and services they will continue to buy, taking price increases into account. This is because they only have their disposable assets and regularly recurring income available for consumption. Customers usually opt for what they consider to be the best price/performance ratio.

Suppliers at all levels try to circumvent, delay and keep price increases as low as possible in purchasing by means of negotiations or changing suppliers. In sales, the aim is to pass on the price increases that have occurred. Whether this is fully successful depends on the preferences of customers on the one hand and on the behavior of competitors on the other.

In order to remain successful in inflationary times, one’s own company must succeed in interrupting the price increase spiral. Inflation is thus a challenge for all employees, because all functional areas are affected, and above all the entire management. Countless ideas for improvement have to be generated, evaluated and decided upon. Furthermore, the interruption of the inflation spiral has to happen quickly, because otherwise the financial result will suffer. Above all, the following must be adjusted:

The assortment to be offered and the assortment width

The pricing process from gross price to net revenue

The marketing, customer acquisition and sales processes

The distribution channels and the definition of target customers

The product development and design

The manufacturing processes and the input materials to be used

The purchasing process and the choice of suppliers

All administrative processes

The data integration and the automation of administrative processes

The investment planning as a result of the process changes.

Professor Simon estimates that most companies can only pass on about 50% of the inflationary cost increases on the procurement side to the customers; the entire cost side in the company must also make a contribution to the profit defense (p. 191).

The next post will go more into detail on which measures have how strong an impact on profits.

In the analysis below the net planned revenues are related to the expected costs of the products, the costs of the planned marketing and sales measures and the necessary investments. This is used to assess whether the entire project will be profitable and can be released for implementation.

This requires a multi-year view, because investments in fixed assets (additional machinery, capacity expansion) are to be expected and the sales volumes as well as the achievable net revenues may change in the course of the project’s life cycle. In addition, it must be taken into account that expenses and costs are incurred at times different than the net revenues. The cash inflows and outflows of the individual years must therefore be made comparable. This can be achieved with dynamic capital budgeting.

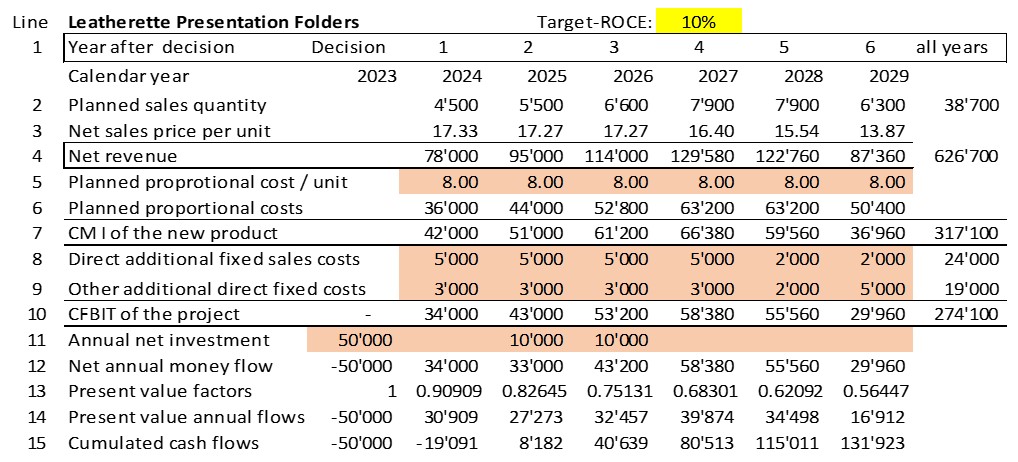

The expected annual net revenues (line 4) are taken from the table on planned sales/revenue development (cf. Costing or Pricing 1).

Since the leatherette presentation folder does not yet exist, the bill of materials and the routing for this product are still missing. As a basis for calculation, the consumption data of a product that is as similar as possible and has already been manufactured can be used. These are supplemented by the expected additional individual material items and production activities. This results in the proportional planned production costs per presentation folder (line 5). If higher purchase prices and proportional cost rates are expected in the years to plan, these cost changes can be taken into account for each planning year. For the time being proportional product costs of 8.00 per presentation folder are assumed in all years. Multiplied by the planned sales quantities (line 2), line 6 shows the annual proportional planned product costs and line 7 shows the contribution to be achieved with the presentation folders in every planned year.

Costing or pricing 2

The annually expected additional fixed costs to be ready to introduce the presentation folder and to generate the annual planned sales quantities are entered in lines 8 and 9. These can be external costs for product-specific advertising, additional costs for the creation of product catalogs, external costs for supplementing the company’s own website and additional personnel costs for the support and administration of the new products. It is important to note that only items that lead to changed cash outflows are taken into account (no allocations).

The result is the annual expected net cash return from the project, i.e. the cash flow before interest and taxes CFBIT (line 10).

The CFBIT is first used to pay for the investments resulting from the project, i.e., additional machinery, capacity expansion of existing facilities, and possibly external rent for additional premises. Higher accounts receivable balances which are expected to follow from the increase in invoiced sales must also be taken into account. If the volume of purchases from suppliers also increases as a result of the new product, the accounts payable balances will increase as a consequence. As a result, the cash outflows only occur in the subsequent period (line 11).

The balance of the annual cash outflows and inflows is shown in line 12.

This line shows that the net cash flows of the years 1 – 3 will be sufficient to cover the new investments and the changes in accounts receivable and accounts payable in years 1 – 3. The payback period of the presentation folders project is a bit more than 2 years.

However, from the point of view of the owners (shareholders) and the lenders (banks), the project should also yield a rate of return in line with the market as they consider whether they should invest their money in Ringbook Ltd. or in another company. To convince the lenders and the owners of the profitability of the project, the management of the company should therefore discount the expected future net cash flows to the moment of the project decision.

For this purpose, the present value of the nominal annual cash flows at the time of the decision should be calculated. Example:

Assuming an interest rate (i) of 10% per annum, a cash return of 1,000 that occurs exactly one year after the project decision has a value of 909.09 at the time of the decision. This results from the discounting formula:

Present value = cash flow x 1 : (1 + i)^1 = 1.000 : 0.90909.

This discounting calculation is done in lines 13 and 14 for each year. The discounted annual cash flows were added up in line 15. The cumulative present value of the project at the end of year 2 is +8,182, which means that the introduction of the leatherette presentation folders will pay for itself after only two years, even taking into account 10% interest.

You can download the generally applicable model for quantifying investments, projects and strategic plans as an Excel model here and adapt it according to your needs.

The market interest rate of 10% used here is up to date for the German-speaking world. In our book 360°-Management, pages 243 ff, we calculated and published the market-driven interest rates of various industries in different countries in 2015. In 2022, it was found that the interest rates stated there are still up to date for German-speaking countries and for the USA.

Conclusion for the financial assessment of plans and especially projects:

Pricing comes before costing: Estimating possible sales quantities and net prices and comparing them with competitor offers is a prerequisite for assessing the profitability of projects.

Separate plans must be drawn up for direct customers and sales intermediaries, as net sales revenues vary widely.

Sales deductions reduce the contribution margin in the same way as proportional product costs.

The direct costs of acquiring new customers must be included in the plan as fixed period costs.

The sales and revenue plans have to be compared with the anticipated proportional product costs of the services and products. The resulting contribution margins I must at least cover the fixed costs of the projects.

The market and the salespersons determine the sales price and the net revenues, not the costs.

Full costs per product unit can be calculated but are not relevant for decision-making because of the fixed cost breakdown.

Feed-forward and feedback are normal in the planning process. It is important to continuously take into account the resulting changes in the plans.

Multi-year horizon: The expansion or contraction of the customer base as well as the company’s own range of products and services always have long-term effects. Therefore, multi-year considerations are usually relevant for decision-making. This speaks in favor of the application of dynamic and money flow-oriented investment appraisal.

Question the assumptions, create and compare several variants of the investment calculation. This makes it possible to include the consequences of different estimates in the decision-making process.