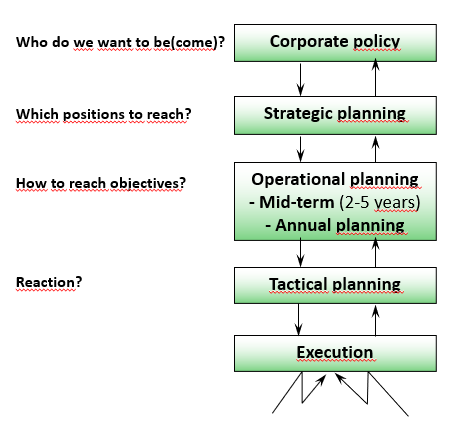

Why the Differentiation between Mission, Vision and Values?

“Sheer Driving Pleasure” is the widely known vision of BMW. It has been valid since 1973 and is also applied to models with electric drive (see https://www.bmw.com/en/automotive-life/the-history-of-the-bmw-slogan.html). This vision is part of the corporate policy.

Purpose, visions, values and generally valid rules of conduct are part of the “corporate policy” planning level. Corporate policy should describe who the company is and/or wants to become.

Because corporate policy is used as a collective term for the self-identification of an organization and for the description of its intended future position, terms such as vision, mission, strategy, rules of conduct and governance are often not clearly distinguished from each other and are not separated from strategy and operation. This in turn leads to the fact that the importance of such statements is not sufficiently recognized within the company.

To clearly assign the various sub-contents of a corporate policy, we use the structure from the St. Gallen Management Model (p. 31 ff.):

Vision: Basic statement for which the company wants to be known and what position it wants to achieve in its area of expansion.

Mission statement: Brief description of the overarching values, rules and lines of development. They apply above all to all employees.

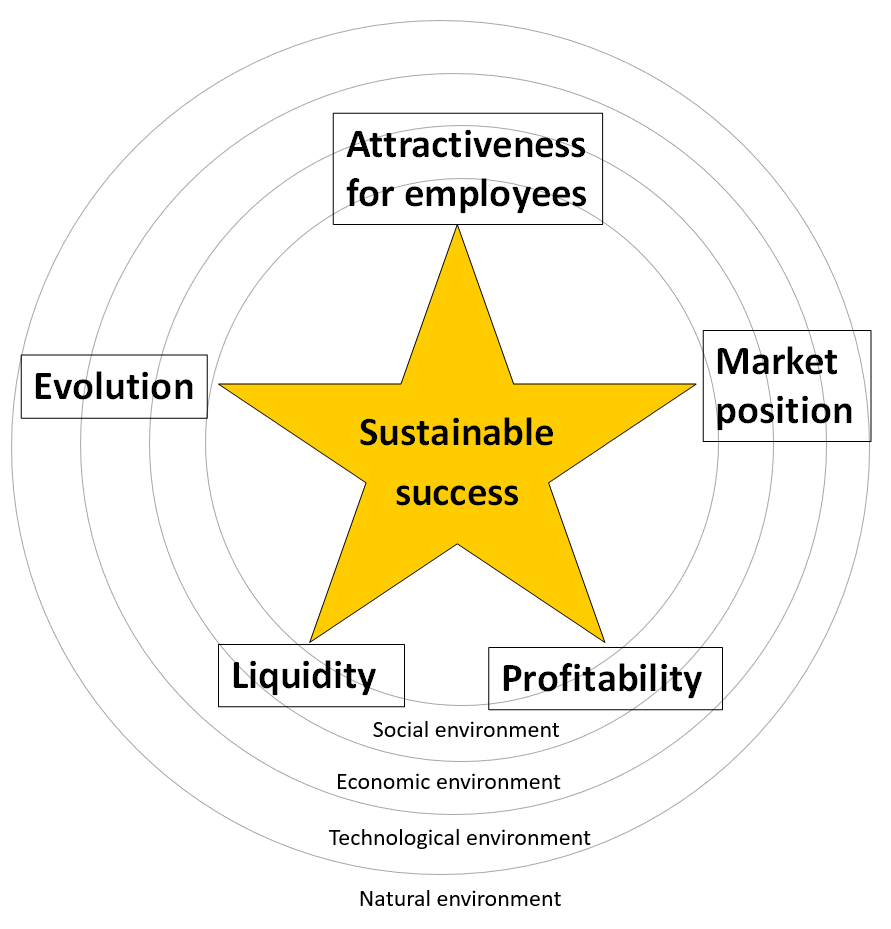

Management concepts: These define the key values to be adhered to and the positions to be achieved in future developments. According to the division into natural, social, economic and technological sub-environments, see the article “Management Control Requires Environmental Reference”), a technology/market-related, an economic and a social concept are to be described. These three management concepts should also specify through which social, technological and economic developments the organization will contribute to the protection of the natural environment.

In his book “Levers of Control, p. 33ff., see bibliograpy” Robert Simons states that every organization is purpose-oriented and that a corporate policy is needed to fulfill its purpose. This policy should contain the core values and beliefs as well as the general boundaries (risks to avoid). Vision, mission statement and the three management concepts thus form the top-level documentation for guiding the behavior of managers, for deriving strategies and for operational implementation (fulfilment of purpose).

“Wacker Chemie AG is a technology leader in the chemical industry, produces for all global key industries and is active in the fields of silicones, polymers, life sciences and polysilicon.”

With this definition, the company describes the product areas it stands for and the industries in which it wants to win its customers.

It is worth studying the corporate policy principles of this group, which has sales of around EUR 5 billion. Their Codes of Conduct can be downloaded as a PDF file from there: https://www.wacker.com/cms/de-de/about-wacker/wacker-at-a-glance/corporate-strategy-and-policy-guidelines/ethical-principles.html .

In our opinion, strategies are not part of corporate policy. They define with which products or services in which markets which positions can be achieved. A company can operate in different markets with different products or services, which means that different strategies can be pursued in different markets. To structure this requires the definition of strategic business units (SBU). Each SBU can pursue an independent strategy but must adhere to the corporate policy guidelines.