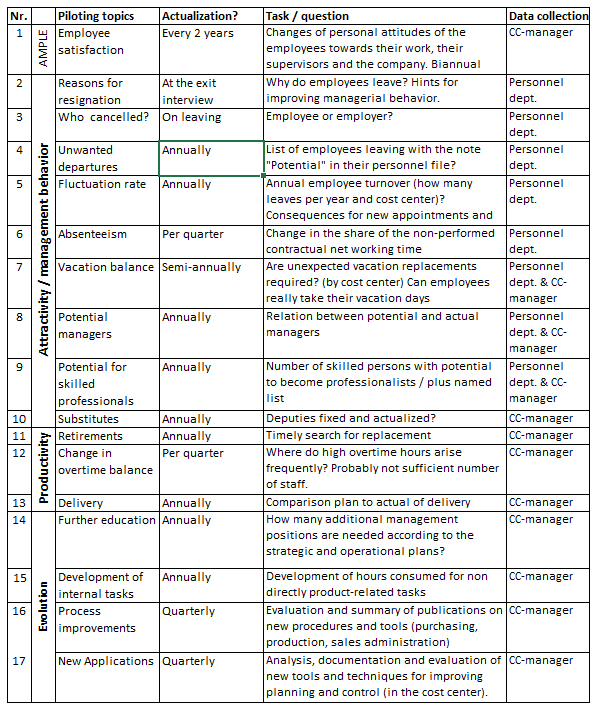

Developing the personnel capacities, abilities and skills is a prerequisite for short and mid-term success.

The management accounting system and the enterprise resource planning system (ERP) contain the performance and value-based data needed for under- and over-year operational planning and control. But building up and maintaining personnel capacities and developing employees’ skills and abilities often requires longer periods of time, either because suitable personnel are hard to find or because specific training and continuing education take longer. Piloting personnel capacities is necessary to have the relevant capacities, skills and abilities ready on time. This requires recording and maintaining various personnel-related data

Piloting Personnel Capacities

Cost center managers (and their supervisors) periodically need to be able to analyze changes in their staff and take them into account in their decisions. In the foreground of such piloting considerations are the top controls Attractive Employer, Evolution and Productivity (cf. the post AMPLE for Sustainable Success). In our opinion, the essential sources for such data are the database of the personnel administration area as well as the personal memos of the managers.

In order to ensure that a management area (cost center) is always ready to perform and that necessary personnel developments are not forgotten, it is advisable to periodically track the following information:

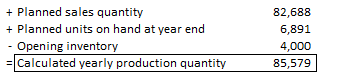

Aspects to consider when deciding on the production and purchase quantities when fixing the yearly plans.

The planned sales quantities result from sales planning. Here, an example from the simulation model is used to show how the production- and purchasing plans are developed.

From Planned Sales to Production- and Purchase-Plans

Item number 101060 is a plastic-coated ring binder with a 4 cm spine width and a 4-ring mechanism. The sales plan envisages selling 82,688 units of these. The following formula is used to arrive at the calculated production quantity:

Calculated planned production

The multi-level bill of materials (BOM) shows how item 101060 is produced:

Bill of materials, tree structure

The production runs in three steps. to produce a 4-ring mechanism (item number 23), a base plate (item number 11) and four wire brackets (item number 14) are required. These articles are semi-finished products. They are not sold as such, but always go into higher level own products. As semi-finished products they are also kept in inventory. Item number 14 is produced in the cost centers Wire rolling and Wire bending & forming. The base plate (item 11) and the wire brackets are assembled in cost center 232 for the mechanism (item 23, production stage 2). The mechanisms are also kept in stock. In the film welding shop and in the assembly department, the mechanisms are then assembled with the ring binder cover (semi-finished product 32) together with further input material to form the final product 101060.

The production planner has the following data at his disposal to determine the planned production:

The data on the planned material requirements for setup and scrap as well as the number of lots to be produced is still missing. These are seized on the basis of measurements in the real production orders and then recorded in the article master as target consumption to be achieved.

Production plan

The defined planned production quantity (in the example 85,800 units) becomes the quantitative basis for the plan-calculation of an item.

It should be noted that a fully automated simulation model can calculate correctly, but it cannot make management decisions itself. The example for determining the planned production shows that management decisions generate new initial values for the simulation. Therefore, it must be possible to capture such decisions in the model or to change the values. This insight also applies to the next stage, the derivation of the planned purchases.

Based on the planned production quantities determined by the production planner, it can be evaluated how much of which raw materials will have to be purchased. For merchandise, the starting point is the planned sales quantity. The table shows the planned requirements for raw materials and trading goods for the planned year, totaled for all items.

The purchasing officer also considers which order quantities he wants to place. This depends first on the planned requirements, but then also on the conditions of the suppliers, such as package sizes, quantity discounts, the most favorable delivery quantity, taking into account the transport equipment and containers of the suppliers and forwarding agents, as well as the company’s own storage capacities. The purchaser will take these factors into account when determining planned purchases. This leads to a break between planned production quantities and planned purchasing quantities, which in turn leads to a break that must be disclosed to the simulation model. To do this, the purchaser should enter his planned purchasing quantities. The planned purchase prices are entered in the article master, since this is accessed when purchase prices are called.

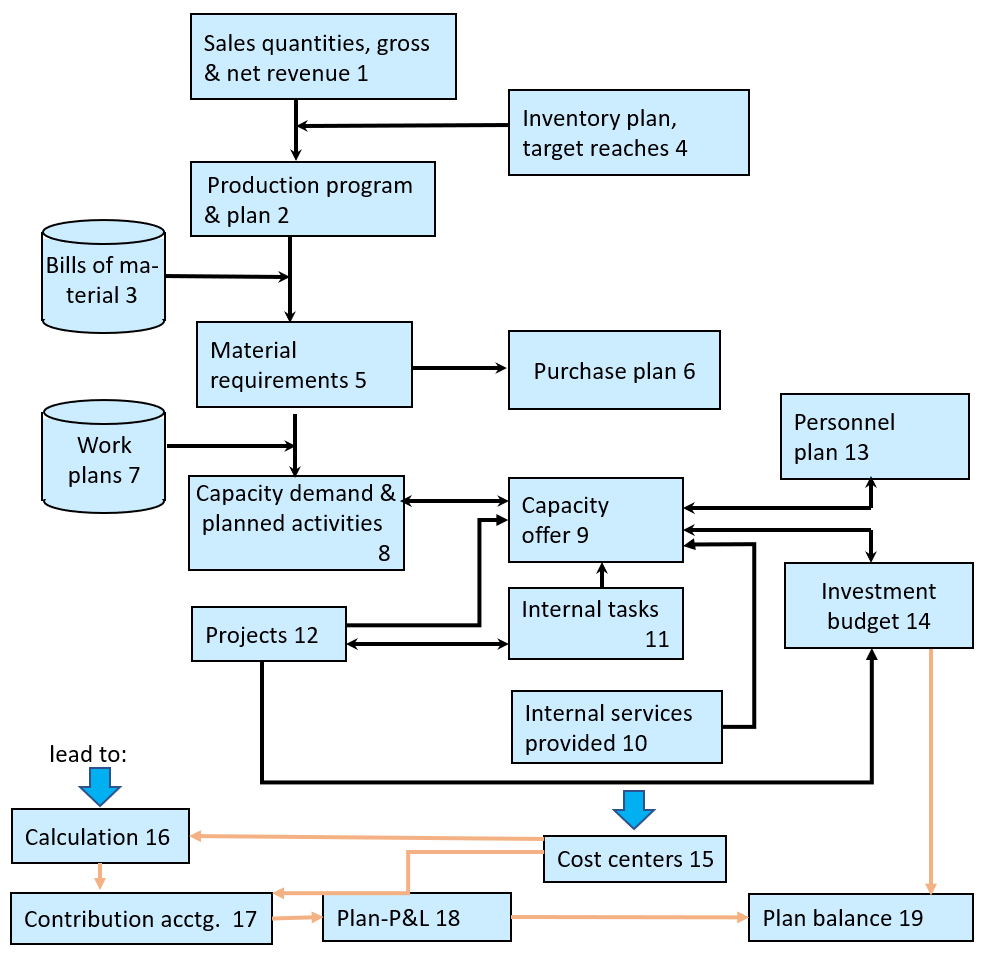

The prerequisite to coordinate plans is to establish the links between them and to know where basic data/information is seized and in which subsequent plans this data is needed.

Integrated planning and control includes coordinating plans because holistic coordination creates a central basis for achieving desired results. For this reason, and in order to derive the detailed requirements for the integrated overall system, the mutual dependencies between the various subsystems of planning are dealt with below.

Starting point are the results from the planned sales volumes and net sales/net revenue (1 in the following exhibit). Using this information, the person responsible for annual production planning derives the production program, also called the rough plan (2). Taking the planned sales quantities per item into account, the task is to determine how many units of which finished product are to be produced.

Planning Dependencies

The following factors play a role in determining this:

Bills of material (3): An example of a bill of material can already be found in the post “Pizza Dough and Management Accounting“. It shows which raw materials have to be provided in what quantities for the pizza dough.

Batch sizes, setup material and scrap (3). These details are also included in the pizza dough example (see respective post). The dough should be enough for four pizzas of 20cm diameter, some flour is needed to roll out the dough and the cuttings that result from cutting into the round shape are actually scrap, which could be used for a small decorative dough figure, but otherwise ends up in the waste.

Inventory targets in terms of quantity, value, and readiness for delivery at any time (4). This is where different interests collide: The production manager wants to be able to produce as large batches as possible so that the consumption for setup and scrap is distributed over as many finished units as possible. The purchasing officer also has an interest in large batches because this enables him to order larger quantities and thus negotiate more favorable purchase prices. The salespersons always want to have enough finished products in stock to satisfy every customer need immediately and thus generate sales. The CFO, however, does not like large lots because he fears that on average there are more units in inventory and therefore more value. The CFO has to finance these stocks with bank loans or capital injected by the owners. In addition, the return on investment (profit before deduction of interest and taxes in relation to the invested assets) looks worse if the profit remains the same but the inventory values increase. The latter makes the company appear less profitable to external observers (bankers and potential investors). The CFO will therefore want lower inventory values.

Based on this discussion, the production planner determines the planned quantity for each item to be produced. This results in the production plan of the year. By multiplying the planned quantity per item with the standard quantities in the bills of material, the material requirements for raw materials and semi-finished products are calculated. Summarized for each raw material, this results in material requirements planning (5). This enables the person responsible for purchasing to negotiate prices and conditions with potential vendors (6). The latter are very interested in concluding annual allotments, because it enables the suppliers to better align their own capacities with the anticipated demand and thus also to produce less costly.

If the quantities to be produced per item are known from the production program, the time requirements can be planned. The prerequisite for this are the work plans (7). In the post Pizza Dough and Management Accounting the individual processes for the production of the pizza dough were also described. The work plan also specifies the working times per process step, which must be observed if skilled workers carry out these operations. In this example, setup and cleanup times are also to be expected, which can be clearly assigned to the product “pizza dough”. The planned production quantities are multiplied by these standard times item by item. The setup times and the allowed processing times for scrap are multiplied by the planned number of lots per item.

By adding up all processing, setup and scrap times, the planned employment of the cost centers directly involved in the production process is calculated. The planned operating capacity is required for cost center planning on the one hand and for determining the personnel plan (13) and machine capacities (9) on the other.

Several service centers usually enable all other cost centers to work at all. Examples are: Workshops, internal transports, energy supply (electricity, steam, compressed air). Their work and costs must also be planned, since they depend on the requirements of the cost centers receiving them (internal services provided (10)).

The necessary working hours and machine capacities for the planned projects (12) are planned accordingly.

Internal tasks (12) include all activities necessary for the upkeep of an organization but their consumption is only indirectly caused by the planned production. This includes all management, planning and administrative work including sales, information technology, building and maintenance, personnel administration, and accounting.

The personnel requirements plan (13) and the investments (14) required to implement the overall plan can only be completed at the end of the overall planning process, since the upstream areas determine the requirements.

For the design of the management control system, it should be noted that up to now, without exception, quantities, activities, times, and capacities have been mentioned. Only in management accounting are these units combined with money and value to provide the overall view.

From gross sales price to net proceeds. Considering all the different types of deductions when planning net revenue per item.

The planned sales should lead to invoiced turnover/sales and to the amount that will be available to the company to cover all costs and to make a profit, the net proceeds.

From Planned Sales to Net Revenue

Increasing division of labor between producers and distributors and the pressure on resellers’ margins mean that new types of sales deductions are being invented which reduce net revenue. The following table provides an overview of the more common types of deductions.

From Planned Sales to Net Revenue

The Management Accounting system should be able to fully represent these types of sales deductions in both planning and actual data. To support decision-making, a distinction must be made between deductions (or surcharges) that directly influence the invoiced revenue and deductions that are granted from the net invoiced sales. Item discounts and invoice discounts can usually be assigned directly to the unit sold. Cash discounts, bonuses, and refunds are only determined after invoicing or even after receipt of payment. As a result, the relevant information is only available after monthly reporting, often long after the end of the year.

To ensure that the company does not “present itself too rich” during the year, we recommend recording the sales deductions at the planned rates (standards) and deducting them from the invoiced sales on a monthly basis. In addition, surcharges and deductions that are not directly item-related should be managed as separate “sales-items”, since, for example, a minimum quantity surcharge is usually calculated per order and therefore cannot be clearly assigned to the individual article. This applies analogously to express surcharges or advertising cost contributions.

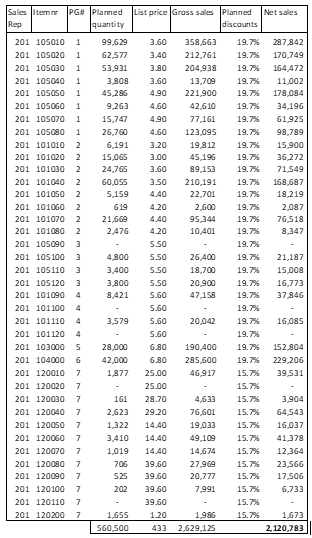

In the simulation model for the example company Ringbook Ltd., item-related discounts are granted from the recommended retail price. These discount rates are determined in planning for each combination of assortment affiliation (own products and trading goods) and customer group. In addition, invoice discounts are granted to encourage customers to place larger orders. These are granted in addition to the item discounts per customer group. Since the list prices and discount conditions are determined centrally, the individual salesperson cannot negotiate his own conditions with the customer.

If the billing documents are available, the invoice and item discounts granted are also known. However, this information is not yet known during planning. For this reason, the average discount rates granted in the prior year per product group are applied in the simulation model while planning.

In the example of Ringbook Ltd. no sales deductions based on invoiced sales are planned. Therefore, net sales also correspond to net revenue. The presented planned sales quantities and net sales are used in later posts concerning production planning and profitability analysis.

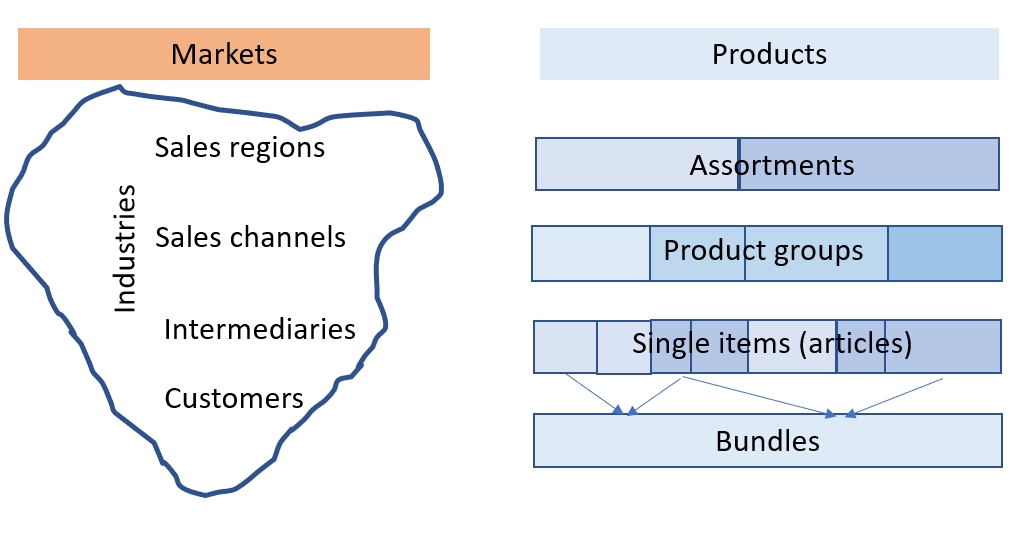

Planning sales quantities in several market dimensions is the consequence of multi-dimensional market cultivation. How to get down to the units to be sold next year?

Planning from Market into Company

An organization’s strategy defines with which products or product groups it will produce, and what positions in which markets are to be achieved (see the post “Strategy and functional concepts“). This applies not only to physical products, but also to services.

Operationally, the sales quantity and revenue objectives to be achieved for each planned year are derived from the strategy and defined for each year. Based on these targets, the quantities to be produced or purchased are to be determined for each item to be sold. This planning can take place at various levels of granularity, for example, by assortment, by product group or by individual item number. It is worthwhile to plan at the level of the single item number as this allows production to better adapt its capacities to the expected demand. However, this detailed planning per item often involves a huge amount of work that the sales staff cannot accomplish. In such cases, statistical distributions based on the experience from previous years come into play.

To improve the planning quality “the markets” should be subdivided into finer sections since demand depends on the market structures, the market potential available in them, and on the stage of development of the submarket itself. It is customary to break down the sales markets geographically by country and, within this, by sales region. Sales channels are also becoming increasingly relevant, for example, direct sales, sales through dealers or agents, and online sales. Sales intermediaries like architects, medical doctors, engineers, nutritionists and increasingly influencers on social media more and more also have an influence on the purchasing decision of an end customer. This development is becoming an important impact with consequences for market cultivation as well.

To plan sales quantities and planned gross revenue by item today means to link three dimensions: Strategy, sub-markets, product structures. Shown as an example:

Planning from Market into Company

Even in small companies, this multi-dimensionality leads to extensive tables. In the example of Ringbook Ltd., four sales region managers, each responsible for their area, are to determine the planned sales for 42 individual items. This already results in 4 x 42 = 168 entries, which can then be totalized according to product groups and assortments. This does not yet take the market dimension into account. Each of the 50 customers can buy the 42 items, what would result in 2,600 possible planning entries. As the sales staff cannot look after his customers while planning, less sales are the consequence during the planning period. Sales management of Ringbook Ltd. requires that each area manager plan the sales quantity per product group for the year to be planned. This requires seven entries (yellow = input fields). As an initial basis for setting his sales targets, the planner reviews the previous year’s sales (12 last complete months).

By using billing data , the previous year’s shares of the individual items per product group can be calculated. The resulting percentages are multiplied by the planned sales quantity of the product group. The result is the calculated planned sales quantity by item and sales area:

For the sales representatives, this planning is part of fixing their next year’s objectives with their sales manager. The representatives must therefore also have the opportunity to adjust the calculated planned quantities to be sold for each item autonomously. This is because it is possible that a product that was not sold in the area in the previous year will be in demand in the future. New customers may be added, existing customers may give up their business or be taken over by other companies. Therefore, the sales representatives can still change the planned quantities of the single items in their final presentation. The procedure is shown in full detail in the simulation model of the book Management Control with Integrated Planning.

If all sales region plans are combined, the result is the sales quantity plan for the entire company. The top sales manager is responsible for achieving this. The detailed sales plan forms the basis for net revenue planning and for determining the planned production quantities.

The Master Plan for Integrated Planning and Control is the IMS

The Integrated Management System (IMS) represents the various elements and subsystems of comprehensive planning and control with their interdependencies. Fredmund Malik developed it based on the St. Gallen Management Model (SGMM). The IMS shows which subsystems and elements are necessary and sufficient for correct and good management. The IMS presentation presented here is slightly adapted to facilitate access to the design of the integrated information system. However, the original content was not changed.

The management topics and the necessary tools are presented in four quadrants.

The Master Plan for Integrated Planning and Control

In quadrant 1, top left, the planning or management levels can be seen, which range from the purpose of the company to annual planning (see “The Main Questions of Each Planning Stage“).

Projects are listed on the demarcation line between company-related and employee-related. This is because real projects usually develop from strategic and medium-term planning. For their realization, the partial results to be achieved in a planned year must be reflected in the personal annual objectives of the assigned project managers and (employees). For space reasons, the box “Projects” is placed in the area above the year. Long- as well as short-range projects should also be included in the personal annual objectives with their milestones (partial results to be achieved).

Organizational structures and processes are derived from the strategic intentions and plans as well as from the functional concepts, which has an impact on operational planning and on the assignment of tasks (functions) and responsibilities. These tasks and responsibilities can be documented with the functional diagram (see glossary).

The realization of strategies and functional concepts requires management capacity. Therefore, both the need for managers and the development of junior managers must be qualified and quantified in the information system (quadrant 3).

Quadrant 4, bottom right, shows how the annual objectives of individuals are translated into results. With management by objectives, personal goals and orders are derived from higher-level objectives or projects. The principles of delegation and self-organization are also included in the implementation path. This results in responsibility for achieving objectives and enabling self-control (see page “Management by Objectives”). Management Control depends on the documentation of objectives in the information system and on the ability to track results achieved according to quantities, qualities, deadlines and results QQDR.

Performance appraisal provides feedback of the results achieved to the person or management function in quadrant 3. Questions regarding the need for technical and managerial competencies must also be addressed there and considered in the multi-year planning. The additional managemers to be recruited and trained are in turn a prerequisite for achieving the strategic and operational objectives defined in quadrant 1.

In quadrant 2, bottom left, the tactical control of the achievement of objectives takes place during the year. For this purpose it is necessary to map all processes and structures of the company in databases. On the one hand, the data must be contained in the information system as planned values so that the plan-calculation can be created. On the other hand, the real events must be mapped in terms of quantity, time and value down to all details that determine results and are relevant to decision-making. At this lowest level (customers, products, individual processes, purchased materials, operating materials and services, and existing plants), the database for integrated planning and control is created. Planning and recording at the lowest level is also indispensable because the data must be able to be evaluated multidimensionally and condensed into higher generic terms.

This information system is usually implemented with the help of an ERP (Enterprise Resource Planning) system. Fully developed ERP systems range from customer acquisition to research and development, from merchandise management and production to wage administration, asset management, internal accounting and bookkeeping. This enables them to cover the requirements of annual planning and tactical control for plan, target and actual.

Finally, controlling is the entire process of defining objectives, planning and control in the financial and performance area (see “Management, Controlling, Controller“). With the help of feedforward (corporate policy and strategy) and feedback (comparison of what was achieved with what was planned), managers try to prepare corrective actions that determine the future, decide on their realization, and subsequently assess the extent to which they have already been successfully implemented. Findings from the controlling process can have an impact at all planning levels. The controlling process is thus placed overlapping both left quadrants.

The personal annual objectives are exactly in the middle of the integrated management system because they describe the results to be achieved by the individual (manager) in the planned year in a measurable or verifiable form. To enable these persons to assess the progress they have made towards achieving their objectives (self-control), the ERP system should provide the database to generate regular plan-to-actual comparisons.

In this blog, the IMS forms the blueprint for the design of the integral management control system.

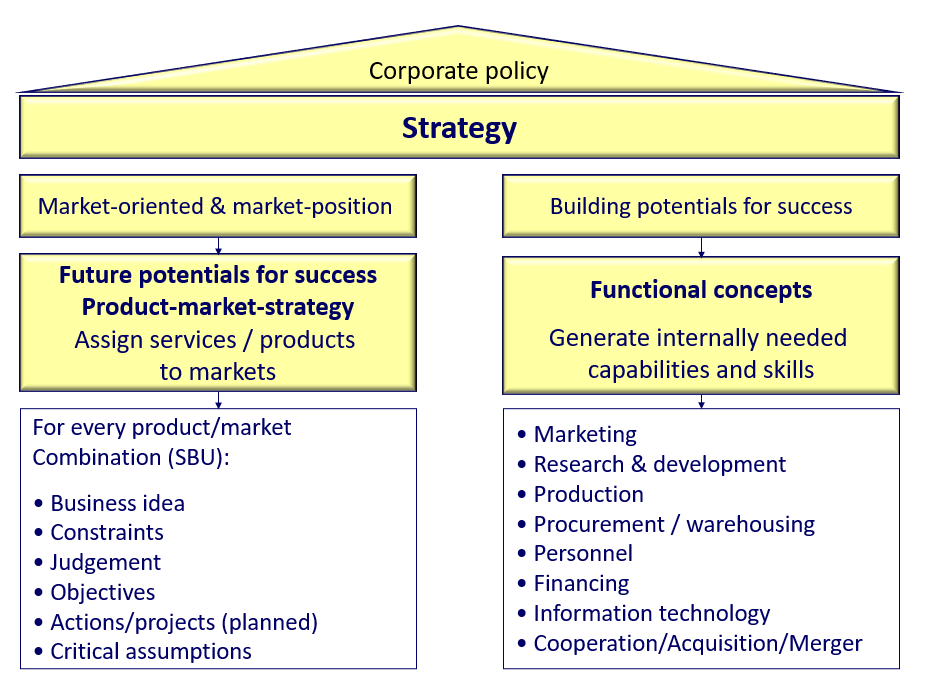

Strategy is outward looking. It determines the unique selling propositions of the offering and the market position to be achieved. Functional concepts are concretized in operational medium-term plans. Their implementation is intended to create and provide the internally necessary success potentials for strategy realization.

Michael Porter (On Competition, 2008) notes that a strategy should describe the unique selling propositions and the market positions to be achieved in the respective market areas with the company’s own offers. This means that an independent strategy must be defined for each product/market combination. Following this definition, objectives, projects and measures must be determined which appear suitable for achieving the desired position operationally.

Unfortunately, the term strategy is nowadays used for almost everything that is associated with planning. This fuzziness in the use of the term leads to uncertainties in management and to poor investments. For this reason, we distinguish between strategies and functional concepts in strategic planning:

Strategy:

Definition of the position to be achieved by independent product/market area and description of the success potentials to be built up or expanded in the areas. This requires the creation of Strategic Business Units (SBUs). For each product/market strategy, the business idea to be pursued, the general conditions to be considered and the responsible persons assessment of the chances of implementation must be specified. As a basis for subsequent implementation planning, the results to be achieved (sales, turnover, deadlines, contribution margins) must be quantified and the most important actions/projects must be fixed.

In addition, the assumptions made in the preparation of the strategic plan, in particular regarding the development of demand and the actions of competitors, must be documented. These can change during the course of strategy implementation, which could lead to a strategy revision.

To be able to check later on whether the original assumptions still apply when comparing the planned to the actual strategy, the assumptions critical to success must be recorded during strategy formulation. We recommend dividing each strategic plan into six parts (see Controller’s Guide, p. 600):

1 Basic idea: Verbal description of the product/market combination to be created and the objectives to be achieved (sales, turnover, contribution margins) as well as the main competitive advantages and customer benefits from the customer’s point of view. 2 General conditions: Description of the factors and conditions in the environments that are important for strategic success but which cannot be changed by the company itself. 3 Assessment: Assessment of the chances of success of the strategic business area, taking into account possible actions of the competitor strategy and possible SBU’s own defense measures. Documentation of the compliance of the strategic plan with the corporate policy guidelines. 4 Objectives: Definition of the qualitative and quantitative benchmarks to be achieved for each year in the strategic horizon (market shares, product range, quality (from the customer’s point of view), incremental contribution margins). Review by means of a dynamic investment calculation (see the menu position “Free Downloads”, Excel template). 5 Action program: List of projects, market cultivation measures, developments in the sales organization and other actions with milestones, responsibilities, decision-making powers and budgets). 6 Critical assumptions: List of assumptions made for market development. If these assumptions are not met, the strategy must be revised or terminated. Other relevant criteria for the continuation decision may be legal changes, political shifts and new competing products or applications.

To enable strategy implementation, success potentials must usually be newly established or expanded within the company. These success potentials are increasingly planned and realized in the functional areas and also across departments. They form the starting point for the definition of functional concepts.

Strategy and Functional Concepts

Functional concepts:

Functional concepts are medium-term objectives and plans of the functional areas for the creation of the success potentials necessary for strategic success. They are defined, for example, for procurement, personnel, production, research and development, information technology (IT) or financing. They create the internal prerequisites for the strategies to be implemented.

For this purpose, plans and projects are created for each area with their results to be achieved, milestones, investment budgets and cost plans and documented in the medium-term planning. Cross-departmental coordination is decisive for success because many results can only be achieved through cooperation. Examples include developing junior managers, developing new applications, centralizing master data maintenance and integrated planning and control systems.

Functional concepts are part of operational multi-year planning because the development of success potentials and integrated processes is often very complex and often takes several years to complete.

Examples of good documents on corporate policy, demarcation between policy and strategy. Content-related elements of a corporate policy.

Why the Differentiation between Mission, Vision and Values?

“Sheer Driving Pleasure” is the widely known vision of BMW. It has been valid since 1973 and is also applied to models with electric drive (see https://www.bmw.com/en/automotive-life/the-history-of-the-bmw-slogan.html). This vision is part of the corporate policy.

Purpose, visions, values and generally valid rules of conduct are part of the “corporate policy” planning level. Corporate policy should describe who the company is and/or wants to become.

Because corporate policy is used as a collective term for the self-identification of an organization and for the description of its intended future position, terms such as vision, mission, strategy, rules of conduct and governance are often not clearly distinguished from each other and are not separated from strategy and operation. This in turn leads to the fact that the importance of such statements is not sufficiently recognized within the company.

To clearly assign the various sub-contents of a corporate policy, we use the structure from the St. Gallen Management Model (p. 31 ff.):

Vision: Basic statement for which the company wants to be known and what position it wants to achieve in its area of expansion.

Mission statement: Brief description of the overarching values, rules and lines of development. They apply above all to all employees.

Management concepts: These define the key values to be adhered to and the positions to be achieved in future developments. According to the division into natural, social, economic and technological sub-environments, see the article “Management Control Requires Environmental Reference”), a technology/market-related, an economic and a social concept are to be described. These three management concepts should also specify through which social, technological and economic developments the organization will contribute to the protection of the natural environment.

In his book “Levers of Control, p. 33ff., see bibliograpy” Robert Simons states that every organization is purpose-oriented and that a corporate policy is needed to fulfill its purpose. This policy should contain the core values and beliefs as well as the general boundaries (risks to avoid). Vision, mission statement and the three management concepts thus form the top-level documentation for guiding the behavior of managers, for deriving strategies and for operational implementation (fulfilment of purpose).

“Wacker Chemie AG is a technology leader in the chemical industry, produces for all global key industries and is active in the fields of silicones, polymers, life sciences and polysilicon.”

With this definition, the company describes the product areas it stands for and the industries in which it wants to win its customers.

It is worth studying the corporate policy principles of this group, which has sales of around EUR 5 billion. Their Codes of Conduct can be downloaded as a PDF file from there: https://www.wacker.com/cms/de-de/about-wacker/wacker-at-a-glance/corporate-strategy-and-policy-guidelines/ethical-principles.html .

In our opinion, strategies are not part of corporate policy. They define with which products or services in which markets which positions can be achieved. A company can operate in different markets with different products or services, which means that different strategies can be pursued in different markets. To structure this requires the definition of strategic business units (SBU). Each SBU can pursue an independent strategy but must adhere to the corporate policy guidelines.

OKR and MBO are central instruments for achieving management success.

Ideas are simple, implementation is everything! This is the mantra of John Doerr, the consultant of Google and other successful companies who introduced the OKR system and sees it as the basis for sensational success in development and results (see: J. Doerr, OKR Objectives & Key Results, 2017).

Ideas are simple, implementation is everything! OKR

In his book, Doerr uses numerous real examples from global corporations as well as small companies to demonstrate that consistent goal orientation is an indispensable key to sustainable success.

The concept of leading with goals is not new. Peter Drucker already laid the foundation for this approach in his publication “The Practice of Management” as early as 1954. George Odiorne described the theoretical concept of Management by Objectives (MBO) and concretized the practical implementation in “The Human Side of Management (1987)”. It seems important to us that Odiorne recognized that the successful application of the MBO system only occurs when objectives are not set by a superior but are transformed into a cross-hierarchical agreement on objectives. Doerr came to the same conclusions (OKR Objectives and Key Results, p. 10).

According to Doerr, an objective determines the “what?”. Objectives should be aggressive and yet realistic, tangible and unmistakable. Their achievement should represent a clear added value for the organization (cf. ibid., p. 226). The SMART formula attributed to P. Drucker (specific, measurable, actively influenceable, realistic and terminated) means almost the same in terms of content.

Key Results express milestones with the associated results. The latter must be measurable, be it with key figures or with documented results (OKR, p. 226).

Management by agreeing on objectives has been an integral part of our management control systematics for years. We are therefore very pleased that Doerr, with his examples from the practice of successful companies, brings two elements to the fore: The objectives must be agreed upon so that the results to be achieved by the individual actors fit in with the overall objectives of the organization and each objective must be defined in a measurable or at least verifiable form. Every manager will confirm from his experience that finding objectives is relatively easy, but realizing them is very exhausting.

In our opinion, objectives, their metrics and the results achieved should be documented in the management control system. Google even goes so far as to allow every employee to see all objectives, including those of his colleagues, bosses and even the executives.

Management by agreeing on objectives is completely interwoven with the management cycle in the integrated management system, since the latter also serves to determine the results and to look for corrective measures if a goal has not been fully achieved. In the various planning or management levels (corporate policy, strategy, operational management) it is also necessary to agree on objectives, to provide the necessary resources and, in accordance with the management cycle, to analyze whether the intentions have become results.

These interrelationships are consequently also determinants for the design of the management control system.

Objectives are results or states to be realized. Therefore they must be formulated in a measurable or at least verifiable way.

No Objectives / no Success

An athlete wants to finish the next competition as one of the three best. If he reaches rank 3 or better, he is successful. An efficiency target of 3% is agreed in a production. It is achieved when the production costs per unit are at least 3% lower than in the previous year.

It is necessary to define the results to be achieved as objectives in order to be able to judge whether a target has been achieved at all. Objectives are results or states to be realized. Therefore they must be formulated in a measurable or at least verifiable way.

Target contents and target levels must be agreed. On the one hand, an objective should be a challenge for the person taking over and, on the other hand it should be achievable with effort. Target setting “from above” causes a defensive attitudein the person whose goal is being set and is hardly accepted.

Objectives should primarily be formulated for a planned year. This makes them easier to coordinate with the annual planning and it can be monitored during the course of the year to see how far the achievement of objectives has already progressed. Corporate policy, strategic and medium-term objectives form the basis for agreeing on annual objectives. The latter are also to be formulated as conditions or results to be achieved.