If you do not improve your cost position, your competition can overtake you.

Part of the consumer experience is that products, ignoring price changes due to inflation, are offered cheaper per unit over time, or that greater performance is offered for the same price.

Some examples:

In 1983, the Motorola Dyna Tac 8000x became the first commercially offered cell phone to hit the market at $3,995. Thirty years later, a cell phone with more features and no ties to a service provider can be purchased at a specialty retailer for about $20, or roughly 5‰.

The original IBM personal computer was introduced to the market in 1981 at a price of $1,565. Thirty years later, PCs were available for purchase for well under $100. These were also much more powerful than the original and offered more features. The HP LaserJet printer hit the market in 1984 at a price of $3,495. After about 30 years, laser printers were on sale around $100.

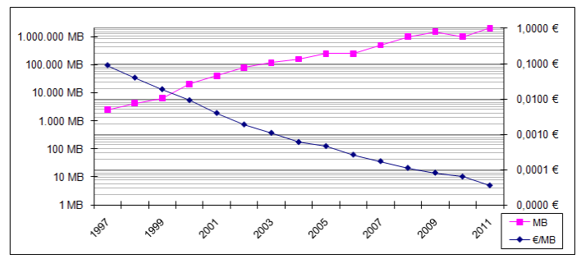

In https://winhistory.de, the development of the sales prices per megabyte of hard disk capacity from 1997 to 2011 is shown:

Development of the sales prices per megabyte of hard disk capacity from 1997 to 2011

The fact that more output is offered for the same price over time can be observed in many areas of the economy. The main reasons for this are technological improvements, competition, and rising production volumes.

Improve cost position

A company must continuously strive to reduce its average total cost per unit of output. If it does not manage to do this, its existing or new competitors will do so, worsening its market position as well as the sales opportunities of the company.

A rapidly and continuously improved cost position is therefore a key prerequisite for achieving or maintaining a strong market position. Companies must be able to substantially reduce their average per unit costs of goods over time if they want to parry sales price reductions by competitors and maintain their profitability. Some of the companies that have managed this balancing act have become global corporations. Many others had to give up because they were not able to reduce the cost per manufactured unit to a sufficient extent.

These relationships have been known for a long time. As a result of his empirical investigations, B.D. Henderson presented the law of experience – also known as the experience curve or Boston effect – as early as 1974 (cf. B.D. Henderson, die Erfahrungskurve in der Unternehmensstrategie, Frankfurt/New York, 1974).

In the following posts, the determinants of the experience curve are first analyzed. It is then shown how the concept of the experience curve can be integrated into one’s own planning and control. The focus is on the alignment of internal objectives with external market developments.

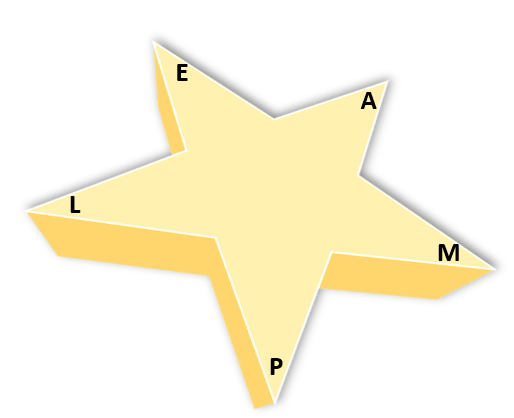

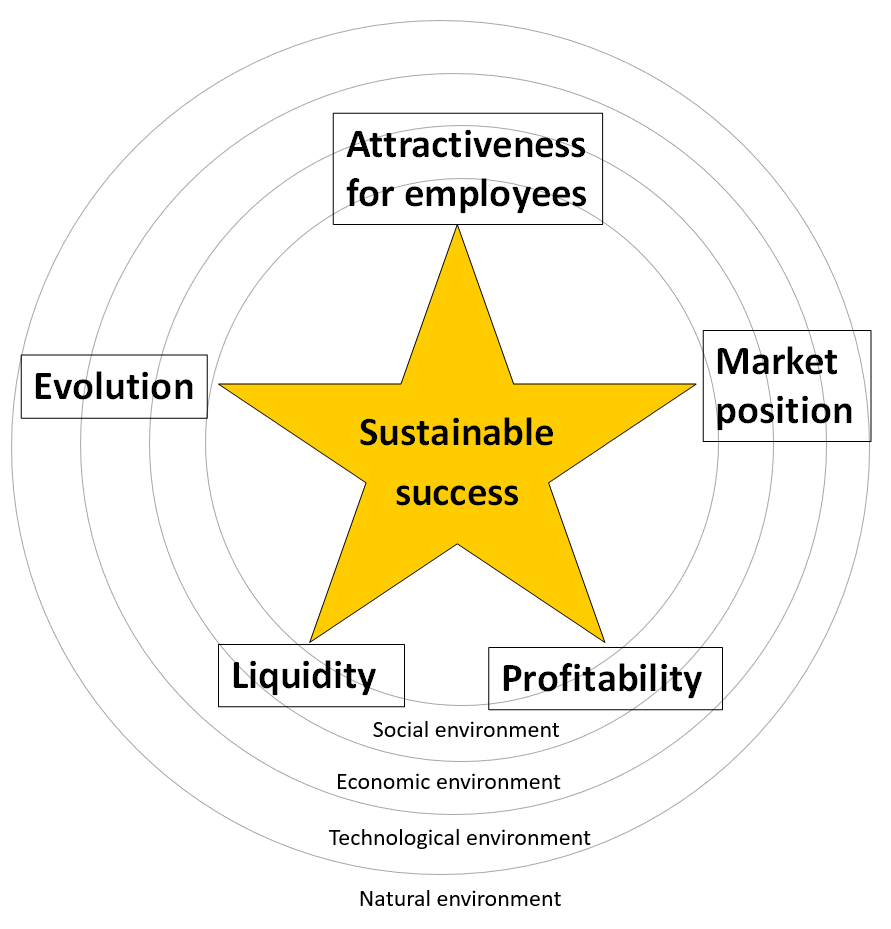

We understand coordination as the alignment of processes to achieve a result on time. Decision-makers and implementers in an organization coordinate objectives, capacities, available resources and the rules of conduct of all participants in such a way that the overall organization acts successfully in the long term and meets the relevant customer and environmental needs. This work takes place within the body of the AMPLE-star.

Coordination of the 5 top-controls Attractivity, Market Position, Profitability, Liquidity and Evolution

Coordination takes place in more or less detailed structured processes.

Examples of highly detailed processes:

Receipt, processing and execution of a customer order

Triggering, processing and measurement of a production order with final stock receipt

Placing an order with a supplier including receipt of the delivery, recording of the necessary data and storage in the warehouse

Preparation of payrolls including posting and payment

Hiring of new employees and recording of all personal and payroll-related data

Sequence of generating, negotiating and deciding objectives.

Less detail is often given to processes that deal with changes in the company’s environments or involve more than one of the 5 top-controls:

Revision of corporate policy and strategic planning

Establishment of research and development priorities

Education and training programs for the workforce and managers

Decisions on marketing and sales promotion programs

Establishment of internal success potentials relevant to the strategies.

Definition of “right of way” rules for decisions affecting several areas, e.g. local sales organization versus central product management.

Coordination is particularly important when decision-making competencies are not fully regulated and/or different interests conflict. This happens during finding and fixing objectives, during implementation, and when corrective measures are defined. To this end, it is advisable to determine in advance which person is to assume the arbiter function. This does not always have to be the next higher superior. Specialized personnel or external persons of trust can also assume this function.

The quality and accuracy of the data required for decision-making is central to coordination. If all parties involved in the decision process receive the same and complete data, this usually creates a clear starting position.

Enterprise Resource Planning (ERP) Systems and related systems such as Customer Relationship Management (CRM), the whole accounting applications and the aggregating management accounting (cost, activity, revenue and profit accounting) should provide the data relevant for decision making. This applies to planned and actual values as well as to the derivation of estimates. Corporate policy and strategic determinations as well as descriptions of the content of plans and projects often cannot be documented in the standard applications mentioned. Spreadsheets as well as text and image-based applications are (still) better suited for this purpose.

Because coordination requires a lot of time, it is advisable to provide time-windows for mutual coordination, especially in the planning calendars (strategic and operational).

Liquidity is essential for the survival of any organization at any time. That is why liquidity is one of the five top-controls (see the post “AMPLE for sustainable success“).

Liquidity

An organization is liquid if it is at all times able to execute all mandatory payments on time. If it fails to do so, it must by law declare its insolvency, which leads to bankruptcy proceedings and in most cases to the dissolution of the organization.

Consequently, solvency must be ensured at all times, both in the short term (day, month, year) and over several years, taking strategic developments into account.

Banks and similar institutions can become insolvent on a more or less daily basis due to large incoming and outgoing payments, because large outgoing payments can occur one or more days before the (re)receipt of expired loans. Thus, in banks, daily tracking of payment readiness planning is essential. In most other companies, monthly planning of cash flows is sufficient.

The scope of insufficient planning, monitoring and control of one’s own liquidity situation in a business context can be seen from the annual analyses of the Austrian credit protection association KSV 1870, https://www.ksv.at/PA%20Insolvenzursachenstatistik%20Unternehmen%202019. As a creditor protection association, KSV analyzes insolvencies in Austria (around 3,000 every year) and classifies them according to cause. The analysis for 2019 revealed the following order of insolvency causes:

42.6% are consequences of operational deficiencies (weaknesses in sales, financing and liquidity, planning and control systems)

Around 21% are consequences of start-up errors (including lack of industry know-how, inexperience, insufficient business training, insufficient start-up capital)

Around 10% are due to neglect of actual management duties.

According to the KSV findings, it is typically the boss who is responsible for insolvency and not the competition or the environment. This result holds true for young companies (up to 5 years old) as well as for longer existing organizations.

These statistically proven findings indicate that regular system-based planning and tracking of liquidity may not be neglected. The impact of short- and medium-term planning of quantities, activities, costs and net revenues on cash flows must be mapped so that correct and informed decisions can be made.

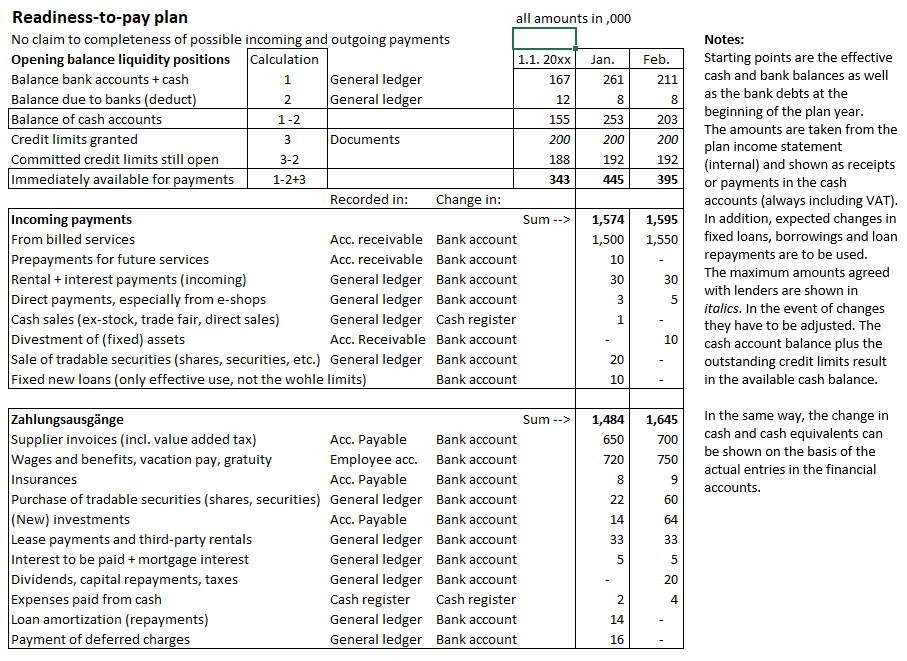

The following example illustrates how, and on the basis of which basic data, a monthly updated readiness-to-pay plan can be created. The initial data are, on the one hand, the immediately available cash and cash equivalents that will be in the books at the beginning of the planned year and, on the other hand, the planned profit and loss statement (planned P&L) of the upcoming year. Their creation can be traced in the simulation model for the book “Management Control System”.

From the planned sales, if the average duration between outgoing invoices and incoming payments is known, it is possible to calculate after how many days the invoiced sales lead to cash receipts (example: on average, customers pay 35 days after outgoing invoices). This means that January sales do not become cash until the second half of February). From the other items of the budgeted P&L, the cash outflows for wages, social benefits, raw material purchases and all other types of expenditures can be derived (the payment period granted by suppliers leads to a later outgoing payment). In addition, there are changes resulting from new investments, increases or decreases in inventories and expiring third-party loans, as well as payments for dividends and other distributions. These can be taken from the budgeted balance sheet (ibid.). A complete example of a willingness-to-pay plan can be found in the “Controller’s Guide”, p. 317ff.

If it is foreseeable that the stock of immediately available cash will tend towards zero, the CFO must ensure that banks or other lenders commit to providing corresponding additional funds. These are usually newly committed credit lines. The company will only use them when it needs them, since they cost interest. Committed credit limits are entered in italics in the corresponding line in the example model. This results in the amount of immediately available cash for each month end after taking into account all cash inflows and outflows of the planned month.

Readyness-to-pay plan

This plan can largely ensure that the organization remains solvent in the planning year. Exceptional situations, especially as a result of a drop in sales, can still occur. The Corona pandemic is an impressive example of this. The planning CFO must therefore consider how large the safety cushion should be to maintain solvency at all times. A proven rule of thumb is that the entire personnel costs including social benefits plus the average accounts payable balance of two months can be paid from the immediately available cash. From the numerical example, it can be seen that this safety cushion does not yet exist. Consequently, the CFO is required to negotiate increased credit limits with the banks.

If the payment readiness plan can be presented to the banks during negotiations for the granting of further loans or for increased credit limits, this increases the chances of success and may help to negotiate more favorable conditions.

However, ensuring solvency at all times must also be taken into account when considering strategic plans with a multi-year horizon. This is because the necessary means of payment depend on the investments, cash-effective costs and net revenues generated by strategic decisions.

Investments in success potentials (mainly additional project costs), inventories and equipment may have to be paid several years in advance, before the sales to be generated lead to cash returns. This requires sufficient cash inflow from owners and usually increased credit limits from banks.

A readiness-to-pay budget on a multi-year basis is sufficient in this case, since the exact payment dates are not known. To prepare this budget, the expected effects of the strategic plans must be reflected in the medium-term planning. These are sales developments, product costs, cost center and, above all, project costs as well as (new) investments in fixed assets and inventories. In order to obtain reliable values, it is recommended that the process of cost center and project planning as well as product costing already be set up in the medium-term plan on a quantity and activity basis. From this, budgeted profit and loss accounts and budgeted balance sheets can be derived, which in turn find their way into the multi-year financial planning. This can be structured in much the same way as the above-mentioned payment plan. The columns then contain the plan years instead of the months.

With the procedure described, shareholders as well as the banks can see which major cash outflows are to be expected and when, and how long it will take until revenues lead to corresponding cash inflows. With this information, management’s prospects of obtaining financing for the planned development on time and on good terms with additional equity and new credit lines increase. Since uncertainties remain despite planning, credit limits with large reserves must always be negotiated.

Overall, it can be seen that volume and performance-based planning is also a central prerequisite for managing the top-control “Liquidity”. The prerequisites for this are created with the holistic management control system. In the book “Management Control System” and in its simulation model, the structure of the required system is described and illustrated, primarily in chapters 4 and 10.

Essential key figures for assessing the liquidity situation are described in the “Controller’s Guide” in chapter 7.3.

Continuous increases in productivity are the prerequisite for increasing profitability within the company.

Profitability refers to earning power, i.e., the ability to generate recurring profits in the short and long term. From a holistic perspective, profitability has two main elements: profitability and productivity.

Profitability

A ratio of two value measures, e.g., earnings before interest and taxes (EBIT) divided by assets used to generate EBIT (return on assets or return on investment ROI). Because in Management Control the inner workings of a company are the starting point, we deliberately refer to return on assets, because it is the use of assets that generates profitability. The return on capital is the view of the financiers.

The ratio ROI tells how many cents of EBIT remain for each EUR invested.

This can also be related to sales: EBIT divided by invoiced sales = return on sales (ROS).

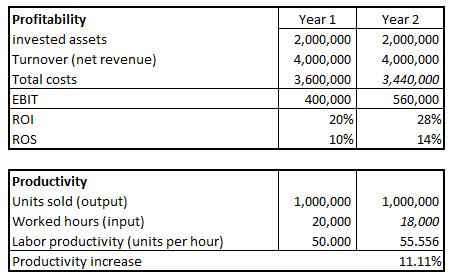

Example:

1 million ring binders are sold at EUR 4 (= 4 million sales) and total costs of EUR 3.6 million are incurred for this, resulting in an EBIT of EUR 0.4 million and thus a return on sales of 10%. If, by improving internal processes in year 2, the number of employee hours to be used, the material input or the costs for machinery and equipment worth EUR 0.16 million can be reduced, the return on sales increases from 10% to 14% and the ROI from 20% to 28%.

Profitability and productivity

Productivity

A productivity metric is a ratio between output and input quantities, e.g., number of units sold divided by the labor hours required to do so in the overall company (labor productivity). Because employee performance, machine input and money input can change the output / input ratio, all factors of the ratio must be made equal. The easiest way to do this is with monetary values.

The productivity increase in the example is 11.11% (for the 1 million ring binders, costs of 3.44 million EUR were incurred instead of the previous 3.6 million, i.e. 11.11% more productive output).

The profitability figures include all input factors (employees, raw materials, external services, equipment) with their prices, which means that price changes in the procurement markets have a direct impact on profitability. Productivity improvements on the other hand show that an output unit was furnished with fewer input means.

It is to be concluded that an organization must concentrate above all on productivity increases if it wants to survive in competition and be sufficiently profitable. In simple terms, it is necessary to look for opportunities to produce and sell more units with the same number of personnel and equipment.

Experience curve

The experience curve provides empirical evidence of the importance of productivity gains. Bruce Henderson (see literature) has analyzed the relationship between productivity and profitability with his empirical studies of input/output-ratios for a wide variety of products and markets. From this he derived the experience curve. It states that with every doubling of the cumulative output quantity, the value-added costs can be reduced by 20 – 30%. This is true for all types of organizations, including public administrations and NPO’s.

Example:

If an organization manages to process 1,200 orders with the same number of staff that is used today for 1,000 orders, productivity will increase accordingly. As a consequence return on sales and return on investment will also be higher.

Productivity increases are always to be sought everywhere. This is because it can be assumed that the competition will also try to reduce the resources used per unit of output in order to lower their value-added costs per unit and thus generate higher profitability.

Realizing the promises of the experience curve means to plan efficiency gains already in medium-term operational planning and to measure in the target to actual comparison whether these have actually been realized. If, for example, an annual efficiency target of 3% compared with the previous year is envisaged, ideas must be found on how to reduce allowed times and material consumption in production and how to reduce personnel deployment per product unit throughout the company. These efficiency objectives are to be stored in the bills of materials, work schedules and cost center plans. The improvements achieved can be measured in the management accounting system.

Presumed developments in the sub-environments are to be well structured for holistic planning and control.

Presumed Environmental Changes are Crucial for Management Control

Every organization is constantly exchanging with its environment. “Out there” are the customers, potential employees, suppliers, financers, the state and other public institutions with their specifications and laws, as well as the social groups with their changing perceptions. All this is embedded in the natural environment.

Sub-environments and AMPLE control

How can environmental factors be structured in such a way that management can relate them directly to its strategic and operational decisions? We use structuring in partial environments (taken from Hans Ulrich, p. 31). Four sub-environments are distinguished:

Natural environment:

This includes everything that happens on earth, including that which is caused by extraterrestrial influences. Although humans can disturb the development of the natural environment, they cannot directly influence it for the good.

Social environment:

Everything that is shaped by behavior, rules and interaction between people. This also includes developments and specifications of governmental and international organizations, changes in interpersonal rules of conduct, changes in mentality and changes in social interaction.

Technological environment:

Changes in sales and procurement markets, new technologies and application areas, and changes in potential competitors.

Economic environment:

Whoever provides financial resources to build or operate organizations wants to be compensated for sacrifycing other investments or consumption. He considers whether his use of funds will be remunerated in line with market conditions. To do this, he weighs the security of the cash or value return against the interest that can be realized with other investments. This in turn depends on the possible compensation of alternative investments and the risk to be taken.

Example topics in the sub-environments

When establishing or expanding a business, opportunities and risks must be identified and weighed up. For this purpose, they must be documented and assessed.

The management control system is the appropriate place to record this documentation and the resulting findings for the management bodies. The four environmental dimensions help to structure, sort and weight the planning statements. They also help to consider all environmental variables when defining the development lines. Examples include:

What influencing factors from the natural environment could make it necessary to adapt our business model? Which elements could make success impossible or, on the contrary spur it on?

To what extent do other structures of living together (e.g., patchwork families, work-life balance, less full-time employment) affect our applied management processes as well as the availability of our employees? Will the increasing density of legal regulations generate higher personnel requirements or even make the profitable continuation of our current business impossible?

Are new application technologies, raw materials and manufacturing processes emerging that will open up new sales opportunities for our products and services? Are there any recognizable saturation or substitution tendencies in the market that could render our existing offerings obsolete? Do new technological standards, e.g., operating systems of computers, require an adaptation of our own products and services?

Are there any developments to be suspected in the customer acquisition process that could jeopardize our sales success to date or are sales intermediaries conceivable who could help to make our products and services better known? Can the concentration of suppliers in saturated markets endanger our existence? Are our competitors theoretically able to produce their products more cost-effectively than we are?

What profitability is to be achieved so that existing equity and debt capital providers continue to invest in our business and – if necessary – new investors can be attracted? What is the degree of self-financing needed to be able to make independent decisions even in periods of low profit and to prevent loan terminations?

In the establishment of corporate policy and strategies a link to environmental developments must be created. In our experience, it is helpful to structure the decisions to be made according to the four sub-environments mentioned. For a more in-depth consideration of the corporate environments, see section 1.1 in the book “Management Control System” (https://management-control.eu/store).