The Management Cycle Determines the Value Types

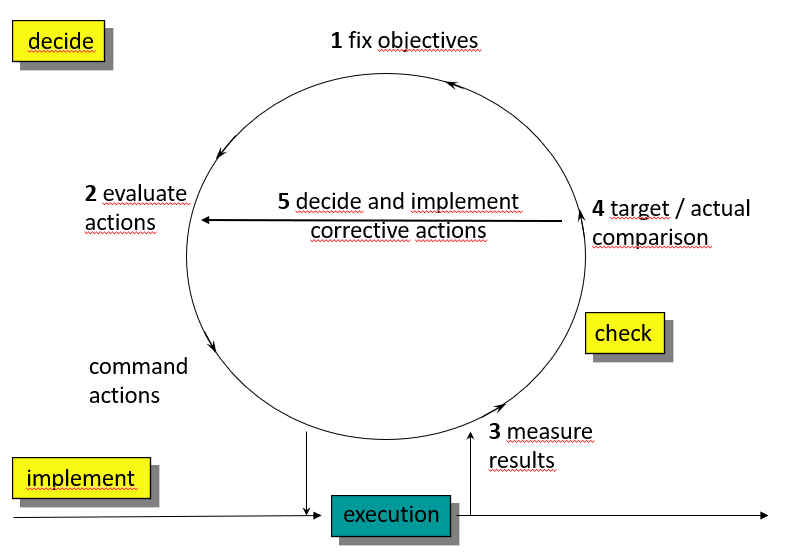

Every manager, whether group leader or CEO, follows the management cycle. He has to plan his area of responsibility. The results they need to achieve must be agreed as objectives with their boss and their own employees in terms of content and deadlines. This requires that target content and target levels be coordinated with the capacities to be provided (people, equipment, money) and with the available knowledge (know how). If investments, process improvements or training are necessary to achieve the objectives, the necessary funds must be budgeted and released. Insofar as project orders are to be provided for this purpose, these must also be planned.

Agreeing on objectives and planning therefore take place in parallel. Their mutual coordination is the prerequisite for the budget resolution (1 + 2).

Plan implementation can be “disturbed” by various internal and external influences. For this reason, the actual results must be measured periodically (3) and compared with the objectives and the plans. This is done in a plan to actual comparison (4). The purpose of this comparison is to find and implement corrective actions (5) which will enable improved achievement of objectives in the next reporting periods.

The integrated planning and control system (IPAC) must be able to map this generally valid management cycle. For this purpose, four value types must be stored in the system:

Plan, actual, variance, forecast (expectation).

Each manager should be able to recognize how well he has succeeded in achieving the plan in his area and what variances have occurred. Starting from the variances he considers which corrective measures could lead to achieving the original plan (and thus also the goal) in subsequent periods. The monitoring process therefore involves not only identifying variances, but also deciding on and implementing corrective measures.

The forecast helps in the management process to assess whether the corrections decided upon will be sufficient to achieve the agreed objectives by the end of the year or project, or whether further measures, possibly in other areas, need to be introduced. It is important to start from the expected effects of the corrective measures when preparing forecasts and not simply extrapolate planned or actual values from previous periods.

Variances in value between planned and actual figures may also be due to the fact that more or less work was produced in a period than planned. In such cases, the responsible manager rightly demands that actual costs be compared with the planned costs of the work actually performed, not with the original planned values. This requires using flexible budgeting in the management accounting system.

Given the requirements resulting from the generally applicable management cycle, management accounting systems adequate for decision-making must be designed in such a way that they:

-

- can present plan and actual figures in quantities, activities and values,

- enable target to actual comparison by valuing actual activities at planned cost rates (“should-be costs”) and comparing them with actual costs,

- enable each manager to enter into the system expected activities and values in his area (usually cost center) for the rest of the planning year or project in order to quantify his expectations (forecast).

From the management cycle It can also be derived that in the plans as well as in the actual analysis, only those items need to be listed that the responsible manager can directly influence and therefore be responsible for. The management accounting system should therefore not allocate fixed costs to cost centers or products if the receiver cannot personally determine the quantity and the content of the service on which the allocation is based (i.e., there should be no fixed cost allocation).