Developing the personnel capacities, abilities and skills is a prerequisite for short and mid-term success.

The management accounting system and the enterprise resource planning system (ERP) contain the performance and value-based data needed for under- and over-year operational planning and control. But building up and maintaining personnel capacities and developing employees’ skills and abilities often requires longer periods of time, either because suitable personnel are hard to find or because specific training and continuing education take longer. Piloting personnel capacities is necessary to have the relevant capacities, skills and abilities ready on time. This requires recording and maintaining various personnel-related data

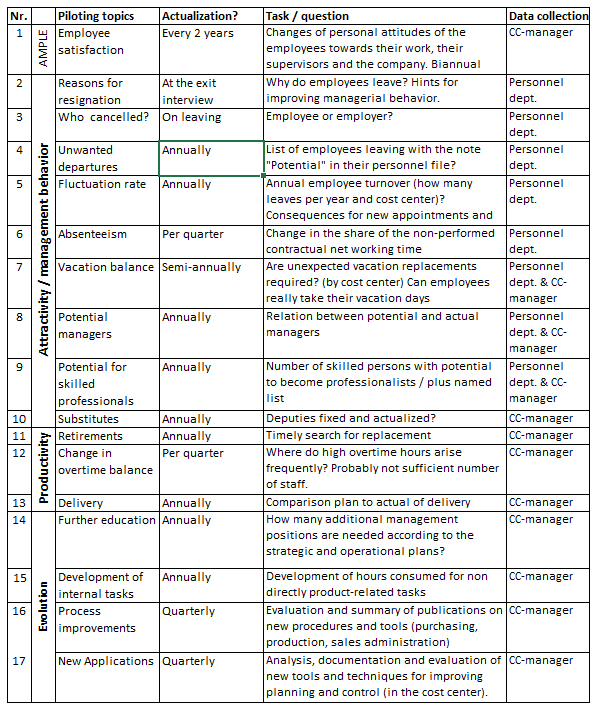

Piloting Personnel Capacities

Cost center managers (and their supervisors) periodically need to be able to analyze changes in their staff and take them into account in their decisions. In the foreground of such piloting considerations are the top controls Attractive Employer, Evolution and Productivity (cf. the post AMPLE for Sustainable Success). In our opinion, the essential sources for such data are the database of the personnel administration area as well as the personal memos of the managers.

In order to ensure that a management area (cost center) is always ready to perform and that necessary personnel developments are not forgotten, it is advisable to periodically track the following information:

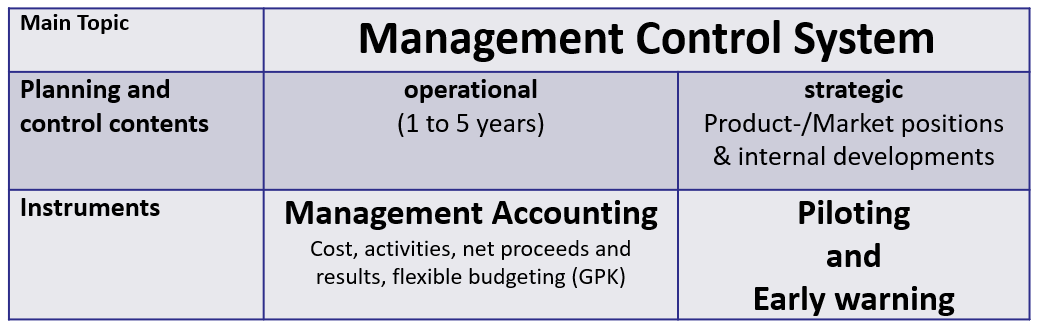

A Management Control System is developed for all managers, irrespective of their hierarchical position. Its purpose is to support decision making and comparison of actuals to plan.

Management Control System Definition

A management control system helps all managers to plan and control in an integrated way. This improves company-wide coordination and the achievement of objectives. It comprises the following subsystems:

Management Accounting + Piloting + Early Warning

Early Warning: Early warning is intended to recognize and structure opportunities and threats in the various corporate environments and, as far as possible, make them measurable. In particular, it is necessary to find out which company-related early warning indicators from the environments can describe significant developments that provide relevant input for strategic and operational planning (opportunities and risks for the future of the company).

Pilot control: To seize opportunities requires the planning company to build up and maintain the necessary success potentials. Strengths can arise from special skills and abilities of the personnel, large management capacity, suitable knowledge for market cultivation, new products and services, advantages through comprehensive process integration or particularly suitable manufacturing facilities. Weaknesses can possibly prevent the translation of opportunities into operational success.

Internal strengths can usually only be built up (or possibly purchased) over a period of several years. For the preparation of operational plans and budgets, parameters are to be found that can measure desired developments in a forward-looking way. Here are some examples: Development of management capacity (number of potential managers in relation to existing ones), development of adherence to deadlines in projects and in delivery readiness, progress in new customer acquisition per time unit.

Insofar as weaknesses in an organization are the result of factual or technical knowledge and application gaps, they can often be mitigated by training and further education or by hiring suitable people. Weaknesses that are rooted in the individual person can hardly be eliminated, especially when employees produce very good results as long as they can work on their own but do not feel comfortable in teams.

In contrast to early warning data, parameters for assessing the development of success potentials (development and expansion of future strengths and reduction of existing weaknesses) are mainly obtained from internal company data. Because the data used for this purpose serves as the basis for medium-term planning, it must be available before the actual operational planning. They are the internal input for planning decisions. This is why we call them piloting factors.

Accounting for management:

In the operational area (medium-term and annual planning as well as tactics (disposition)), plans are more finely detailed and the associated objectives are defined and hopefully also implemented. Accounting for Management is intended to enable managers at all hierarchical levels to translate their plans into objectives for the actual activities and to prepare the target to actual comparisons.

Target to actual comparison is intended to find starting points that will lead to the definitive achievement of objectives in the coming periods (e.g., months). It is created in monetary values so that different consumptions and services can be compared with each other.

This requires a consistently management-oriented cost, performance, revenue and contribution accounting up to Earnings Before Interest and Taxes (EBIT). It must be able to map plan, target, actual and forecast. The data foundation comes from the tactical systems (Enterprise Resource Planning Systems (ERP)) and from ledger accounting.