Bottlenecks at Service Providers

For service providers, material consumption and machine capacity are rarely the key bottlenecks. Mostly the available hours for order-related work limit the achievement of a profit in line with the market.

Activity- and cost-planning for an ERP- implementation

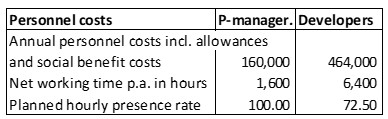

A small IT company implements ERP-systems for its customers and also programs software enhancements as needed. The customers are in each case supported by a project manager. The developers perform the implementation work and also create program adaptations if required. For the plan year, the personnel costs of the project manager and the four developers are as follows:

Personnel costs of IT-department

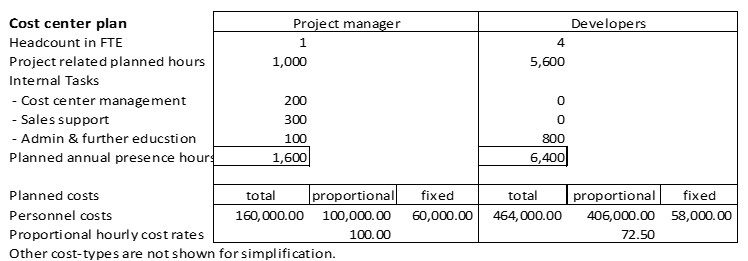

The following simplified cost center plans resulted from annual planning:

If the hours scheduled for Internal tasks (cost center management, sale support, training and internal administration) are deducted, 1,000 hours remain during which the project manager can work on customer orders. The developers plan to work 5,600 hours on projects.

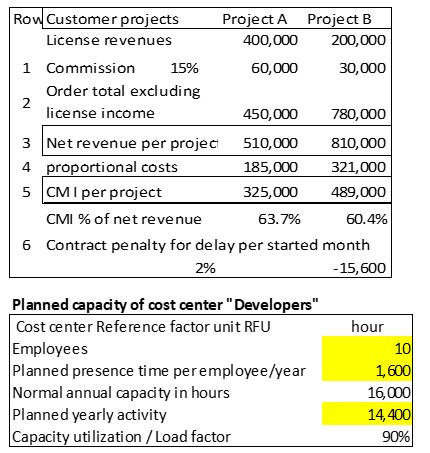

According to project planning, the following hourly employments are foreseen for 2 projects in the planned year (in hours):

The order-related planned hours can be performed for both projects.

Planned contribution margins

The supplier of the standard ERP software grants the installing IT company a commission of 15% of the license revenue invoiced to the end customers (line 1). The contracts with the two end customers include the agreed project manager hours at 250.00 per hour and the developer hours at 175.00 per hour. For each project, this results in the contract total excluding license revenue (line 2). Line 3 contains the net revenues per project.

The planned proportional production costs per order were calculated by multiplying the proportional planned hourly rates of the cost centers with the planned hourly consumption (line 4 below). This results in the CM I to be achieved per project.

To ensure that Project B is fully operational on schedule, i.e. by the end of the planned year, the client insisted that a penalty of 2% of the contract sum (line 6) be deducted from the agreed contract sum per month of late completion.

Personnel bottleneck

On June 30 of the year, one of the developers terminates his employment contract as of September 30 because he wants to continue his education.

As a result 400 developer hours will be missing in the fourth quarter. Both projects should be completed by the end of the year. The search for a new developer has been unsuccessful so far.

The project manager consults with sales management. Two solutions are outlined:

-

- Complete project B only by the end of January of the following year. This would trigger the penalty of 15,600.

- Convince the client of project A that his project will not be completed until the end of January of the following year. For this delay, he would receive a subsequent discount of 25,000.

In purely arithmetical terms, the difference of 9,400 between 1. and 2. argues in favor of completing Project A on schedule at the end of the year and to pay the contract penalty for Project B. If, on the other hand, Project B were not completed until the end of February or even later due to further delays, a further 15,600 penalty would have to be paid each month, which would mean that the one-off discount for Project A would have less impact on the result.

In the real case, other factors not considered in this example calculation would have to be taken into account, e.g. effects on customer satisfaction, adherence to schedules, follow-up orders and the reputation of the IT company.

Cost splitting in service companies too

The example is intended to show that the splitting of cost center costs into their proportional and fixed parts is also relevant to decision-making in the planning and management of service companies. Only if it is known which costs are directly caused by a certain service, it is possible to distinguish which costs are caused by the service units provided and which are the fixed period-dependent service-readiness costs.