The Master Plan for Integrated Planning and Control is the IMS

The Integrated Management System (IMS) represents the various elements and subsystems of comprehensive planning and control with their interdependencies. Fredmund Malik developed it based on the St. Gallen Management Model (SGMM). The IMS shows which subsystems and elements are necessary and sufficient for correct and good management. The IMS presentation presented here is slightly adapted to facilitate access to the design of the integrated information system. However, the original content was not changed.

The management topics and the necessary tools are presented in four quadrants.

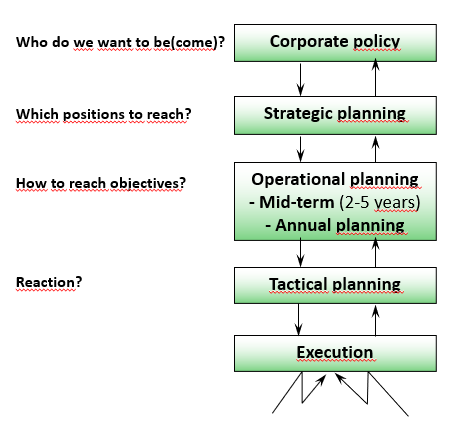

- In quadrant 1, top left, the planning or management levels can be seen, which range from the purpose of the company to annual planning (see “The Main Questions of Each Planning Stage“).

- Projects are listed on the demarcation line between company-related and employee-related. This is because real projects usually develop from strategic and medium-term planning. For their realization, the partial results to be achieved in a planned year must be reflected in the personal annual objectives of the assigned project managers and (employees). For space reasons, the box “Projects” is placed in the area above the year. Long- as well as short-range projects should also be included in the personal annual objectives with their milestones (partial results to be achieved).

- Organizational structures and processes are derived from the strategic intentions and plans as well as from the functional concepts, which has an impact on operational planning and on the assignment of tasks (functions) and responsibilities. These tasks and responsibilities can be documented with the functional diagram (see glossary).

- The realization of strategies and functional concepts requires management capacity. Therefore, both the need for managers and the development of junior managers must be qualified and quantified in the information system (quadrant 3).

- Quadrant 4, bottom right, shows how the annual objectives of individuals are translated into results. With management by objectives, personal goals and orders are derived from higher-level objectives or projects. The principles of delegation and self-organization are also included in the implementation path. This results in responsibility for achieving objectives and enabling self-control (see page “Management by Objectives”). Management Control depends on the documentation of objectives in the information system and on the ability to track results achieved according to quantities, qualities, deadlines and results QQDR.

- Performance appraisal provides feedback of the results achieved to the person or management function in quadrant 3. Questions regarding the need for technical and managerial competencies must also be addressed there and considered in the multi-year planning. The additional managemers to be recruited and trained are in turn a prerequisite for achieving the strategic and operational objectives defined in quadrant 1.

- In quadrant 2, bottom left, the tactical control of the achievement of objectives takes place during the year. For this purpose it is necessary to map all processes and structures of the company in databases. On the one hand, the data must be contained in the information system as planned values so that the plan-calculation can be created. On the other hand, the real events must be mapped in terms of quantity, time and value down to all details that determine results and are relevant to decision-making. At this lowest level (customers, products, individual processes, purchased materials, operating materials and services, and existing plants), the database for integrated planning and control is created. Planning and recording at the lowest level is also indispensable because the data must be able to be evaluated multidimensionally and condensed into higher generic terms.

- This information system is usually implemented with the help of an ERP (Enterprise Resource Planning) system. Fully developed ERP systems range from customer acquisition to research and development, from merchandise management and production to wage administration, asset management, internal accounting and bookkeeping. This enables them to cover the requirements of annual planning and tactical control for plan, target and actual.

- Finally, controlling is the entire process of defining objectives, planning and control in the financial and performance area (see “Management, Controlling, Controller“). With the help of feedforward (corporate policy and strategy) and feedback (comparison of what was achieved with what was planned), managers try to prepare corrective actions that determine the future, decide on their realization, and subsequently assess the extent to which they have already been successfully implemented. Findings from the controlling process can have an impact at all planning levels. The controlling process is thus placed overlapping both left quadrants.

The personal annual objectives are exactly in the middle of the integrated management system because they describe the results to be achieved by the individual (manager) in the planned year in a measurable or verifiable form. To enable these persons to assess the progress they have made towards achieving their objectives (self-control), the ERP system should provide the database to generate regular plan-to-actual comparisons.

In this blog, the IMS forms the blueprint for the design of the integral management control system.