Last Updated on March 12, 2024 by Lukas Rieder and David Moser PhD

The short- and long-term profitability of an organization is increasingly determined by the fixed costs of the supporting functional areas (procurement, human resources administration and development, information technology, facilities, investment and finance, sales and marketing, executive management). As a result of increasing complexity, the costs incurred for these functions are rising continuously. In many companies they are today higher than the proportional product costs. If an organization is to become more profitable, it is therefore particularly important to reduce fixed costs in these areas through Lean Management.

Fixed cost reduction with Lean Management

This is the field of Lean Administration, Lean Logistics and Lean Sales. It is about making the total fixed costs of the organization increase more slowly than the net revenue. The first and most important starting point for this is to reduce or prevent working hours that are used to win and keep customers, as well as for the administration and management of the organization. The second is to ensure that investments for successful further development in all areas (especially IT and buildings) grow more slowly than net revenues, because they lead to fixed operating and depreciation costs.

Lean Administration

Efforts are made to reduce labor input for:

-

- Complying with government/regulatory requirements (primarily personnel administration and compliance with labor laws).

- Maintaining operating permits (documenting legal compliance)

- Documentation of legally compliant functioning of plant and equipment

- Documentation and traceability of product creation

- Recording data and ensuring data quality

- Planning and recording of costs and revenues plus evaluation

- Recording and evaluation of all accounting data

- Performing management duties in all areas to be managed.

Lean Sales

is to ensure that the labor input for the following tasks grows more slowly than the net revenues generated. Of main concern are:

-

- The entire sales and distribution process (from address acquisition (lead) to customer follow-up),

- Travelling time and cost,

- Product management and sales promotion, and

- Advertising and other marketing activities.

Lean Logistics

should ensure that

-

- Raw materials, supplies and other goods and services can be purchased at lower cost (contract design, delivery terms, other materials that also meet the requirements),

- All specifications for goods and services to be procured are available electronically before the ordering process is triggered,

- Transportation costs for delivery and shipment become cheaper per unit,

- The workload for order and delivery processing is reduced,

- All relevant data is available directly and without access to paper files, and

- Procurement processes can be handled in a single pass and without waiting times.

Increased efficiency through higher master data quality and service recording

The master data quality of customer, employee, and supplier data is a priority if search processes and requests for current data are to take up less working time. In our opinion, the availability of up-to-date data at all times is a central prerequisite for the realization of administrative processes that are as waste-free as possible. It remains to be seen whether a company’s master data should be maintained centrally or by department, and who should be responsible for what content.

In all the areas mentioned, the aim is to achieve efficiency gains and thus remain competitive. This requires planning and measuring the work input for the various (sub-)processes. For this purpose, these must be captured in terms of content so that the time worked on internal tasks can be measured. Shop floor data collection as is common in the manufacturing sector must also be applied to the measurement of working times for internal tasks. Many “white collar” workers resist this recording, but only this data makes it possible to measure achieved effectiveness (are we doing the right thing?) and efficiency improvements (are we doing it right?).

Recording of time spent on internal tasks must be done on a contemporaneous basis. After all, tomorrow you no longer know exactly how much working time you spent on which task yesterday. If a suitable electronic recording application is available directly at the workplace, this recording is easy. The post “Capacity requirements for internal tasks” shows how internal tasks can be structured so that their recording and classification is simple and does not take a lot of time.

In Lean Administration projects, the main goal is to reduce time consumption for repetitive work. This requires direct observations and consumption records per work step, as small time savings can be found, which add up to entire full-time positions through repetition thousands of times.

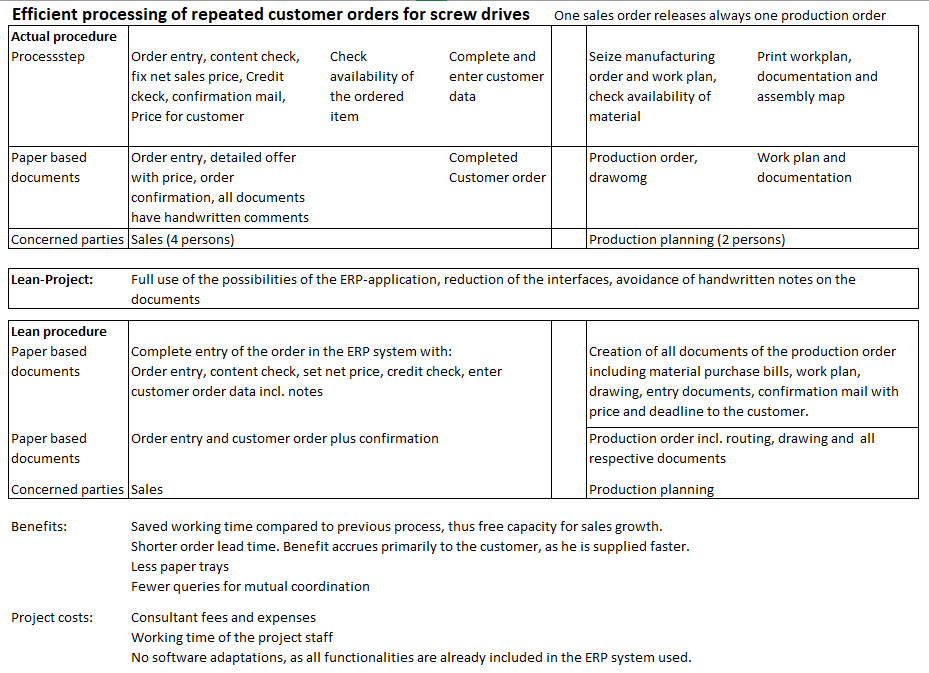

Practical order processing example

In this example from a manufacturing company, the entire process from customer order to delivery and invoicing to the customer was examined. The company wanted to reduce the time required for processing and at the same time shorten the lead time of an order. This was to create free capacity for more customer orders. When the as-is status was recorded, it was found that the turnaround time was 2-8 days; after implementation, it was 1-3 days. The average processing time per order dropped from 40 minutes to an average of 20 minutes, i.e. to about 50%. With around 13,000 orders per year, this corresponds to a time saving of approximately 4’300 working hours per year.

If the staff were to be reduced, a total of 2.5 fewer full-time positions could be planned in the next planning year in the cost centers sales processing and production planning. If the freed-up personnel capacity is shifted to other cost centers, these would have to increase their planned personnel costs accordingly in the next plan year.

David Moser PhD

Dr. David Moser is co-founder and managing partner of Wertfabrik AG. With a doctorate in physics, he has many years of experience, including in the areas of Lean Enterprise, Lean Administration, Shopfloor Management and coaching of executives. Before founding Wertfabrik, he was Managing Director at HARTING AG in Biel/Switzerland and most recently Managing Director and Senior Partner at STAUFEN AG also in Switzerland. Today, the specialist for process optimization is active as a consultant and speaker for numerous industries.